Tagged: Mumbai Female Escorts

- This topic has 5,394 replies, 166 voices, and was last updated 1 day, 11 hours ago by Sobha.

-

AuthorPosts

-

February 4, 2023 at 1:01 pm #25587odyseeRegistered Boarder

@akkithegrt, all subsidiaries are audited. The audit reports and audited accounts of the subsidiaries have not been uploaded by the company on its website although they were provided to Deloitte and SEBI in relation to the ongoing FA as per the last conference call. Hopefully that will get rectified in the not too distant future.

February 8, 2023 at 11:32 pm #25606kmr003Registered BoarderAs investor it deep pain to see, even after fabulous numbers

market is not interested and recognizing the growth story,1. BCG management should understand real growth comes when shareholders value is created . It is high time SKR should change his attitude how to run public company.

2. SKR should appoint credible / trustworthy / experienced management persons to board OR if he is replaced (don’t think it will happen) . I’m sure market will cheer .

3. SKR very slow in addressing the shareholders concerns , I don’t think they are bothered about shareholders wealth eroded in last year.

4.To bring trust in markets,

We should raise concern to appoint big 4 as consolidated auditors ,

Release Audited numbers of subsidiaries.

Consider buy back, ESOP

Promotors share holding issues to be resolved earliest .

Investor meet for DII, and bring some reputed investors to buy5. Every one on social media mocking results. making fun of results as manipulated results . It seriously hurts as investor. Dot know how it is for SKR

Requesting @admin and everyone (telegram) to raise concern to appoint big 4 as BCG auditor in next FY. at least this brings some trust in market

14+February 9, 2023 at 7:11 pm #25607akkithegrtRegistered BoarderThanks @odysee, We know that subsidiaries’ results are audited, but they should be made public. If the audited subsidiaries’ results are not made public, how can investors trust BCG?

Please understand that if more than 90 percent of revenue and profit are coming from subsidiaries, then it is mandatory to make those subsidiaries’ audited results public.

Unless and until audited subsidiaries result are not made public or forensic audit results don’t come, market won’t value the company.

SKR should start taking shareholders’ concerns seriously.

I have no doubts about BCG’s growth over the next five years, but I am concerned about the value BCG will create for its shareholders over the next five years.February 10, 2023 at 8:55 am #25609odyseeRegistered BoarderDon’t disagree at all @akkithegrt. I am a strong proponent of the company meeting its statutory obligations and being completely transparent in all communication with stakeholders.

The auditors’ reports and related financial accounts for all subsidiaries must be uploaded on the company’s website earliest. Just providing the summarised financial results of each subsidiary annually is totally inadequate and does not fulfill the moral and statutory requirements.

Since the full data has already been provided to Deloitte and SEBI, there is no justification in withholding the same from the public, notwithstanding the sensitivity indicated in the conference call pertaining to the Daum settlement.8+February 10, 2023 at 6:00 pm #25610BrightspotRegistered Boarder@odysee how can you believe MR Suresh kumar might have given all the documents? This is not the first time he had given wrong info share holders

Almost 1 year he was telling Mediamint acquisition going extremely well in the conference call then suddenly he informed they have changed their mind

Almost one year they have been telling they are “Acquiring ” all assets of Audio company then suddenly they announced JV

Now I think he dont want to upload subsidiary reports so the delay in duam settlement

its almost 6 months they identified payment method but could not close it, hard to believe.. Directors are incompetent, they will listen whatever SKR ask them to do..thats my view only based on the experience I had since 4-5 yearsThey have to report to sebi every quarter if there is any deviation in using the funds or not,all other companies following that except brightcom

February 11, 2023 at 2:07 am #25611LoganRegistered BoarderAs investors we have done everything we can and now everything depends on the management and the promoters. Some investors have requested while others have complained to SEBI but if the management doesn’t want to act then we can’t do anything. It’s very frustrating to see the stock performing so badly when the company is doing well on the business front.

What other companies’ management people do is they try to clear uncertainties as their company grows but in BCG’s case there’s no improvement and we still feel like it’s being run like a private company.

Except fa all the other matters are fixable from their end. Fixing those may not change everything but at least it’ll give more clarity and remove/clear uncertainty to an extent.

February 11, 2023 at 12:05 pm #25613NikhilrajRegistered BoarderSir ,

As a listed company management have some responsibilities and we investors have some rights to know status of ongoing issues . But management always hide or never tried to adress the issues properly with investor community . Infact they always created a space for creating stories .

We all are so connected through forums and telegram group . Any movement is possible to force the management to do their responsibility in a decent manner ?February 11, 2023 at 8:56 pm #25614BrightspotRegistered BoarderDear Admin and respected member of this forum, I would to request some members of this forum attempt to meet Peshwa who was assigned responsibility to lead Daum closure and ask him what exactly the problem in closing the issue? we can pressurize SKR to upload audited numbers after that..we cant wait until our hard earned money being eroded like this..We need to know how much more time he need to close it, its been 6 months he told us that they have identified payment method to close Daum, I would like to know others view also on this initiative

February 11, 2023 at 9:39 pm #25615NikhilrajRegistered BoarderIn this DAUM settlement also company is not transperant to investors . Some stories says Korean company is asking more money than initially agreed, some stories says BCG plan is to not to clear this settlement as no benefits to company by paying huge amount and making LYCOS a part of company in the current scenario.

Some stories says this issue is almost completed ( we are hearing this for the last many months )..

As an investor what we need is clarity on the ongoing issues . If company is transparent in these issues we investor will have more confidence and can easily defend all the negativities in the social media .

A few of our members had met with SKR 2-3 times and all the promises he gave to them are still promises and not materialized .

At this point of time what we need is clear timelines and not promises .

Company do not have any acquisition plan for organic or inorganic growth with huge cash balance . With mediamint , quantum ,or audio acquisition company followed JV model . So what is the plan with cash balance ?

We should pressurise the management to get clarity on all our queries . Still companies investor relation group is not functioning properly,I feel .February 11, 2023 at 9:48 pm #25616BrightspotRegistered BoarderJust to show regulator that they have taken some action on corporate governance he introduced Call center, however that is useless, they take your name # and email address and send it to IR team and as usual IR team wont reply

I have strong doubt that Daum issue was kept open on pretext to avoid sharing audited number to public5+February 11, 2023 at 9:49 pm #25617BrightspotRegistered BoarderJust to show regulator that they have taken some action on corporate governance he introduced Call center, however that is useless, they take your name # and email address and send it to IR team and as usual IR team wont reply

I have strong doubt that Daum issue was kept open on pretext to avoid sharing audited number to public

They dont need Lycos search engine, its already old no one using it

Mediamint acquisition not happened (there is no communication on failed acquisition from mediamint side until now)

Audio Aquisition reduced to JV

Quantum computing doesnt require huge investment , they have hooked some university professor for itThere is no clarity on using rest of the fund raised for inorganic growth

Is it time to meet again for discussing these things?6+February 11, 2023 at 10:26 pm #25618kmr003Registered Boarder@Rathi_b and team met SKR and had a discussion, Hope it was two months ago.

I personally don’t see any improvement in CG.I don’t think DAUM Settlement will bring stability to price.

Share holders lost the trust on SKR and Management, BCG is least bothered about shareholders wealth eroded in last 1 year,

but BCG still repeating same sentences will improve CG.Now they should work in rocket speed to improve transparency and CG. and take some extradentary steps to bring confidence back

(like clean FA output / Buy back / ESOP / dividends / reputed hires )I personally see only talks on ground no work .

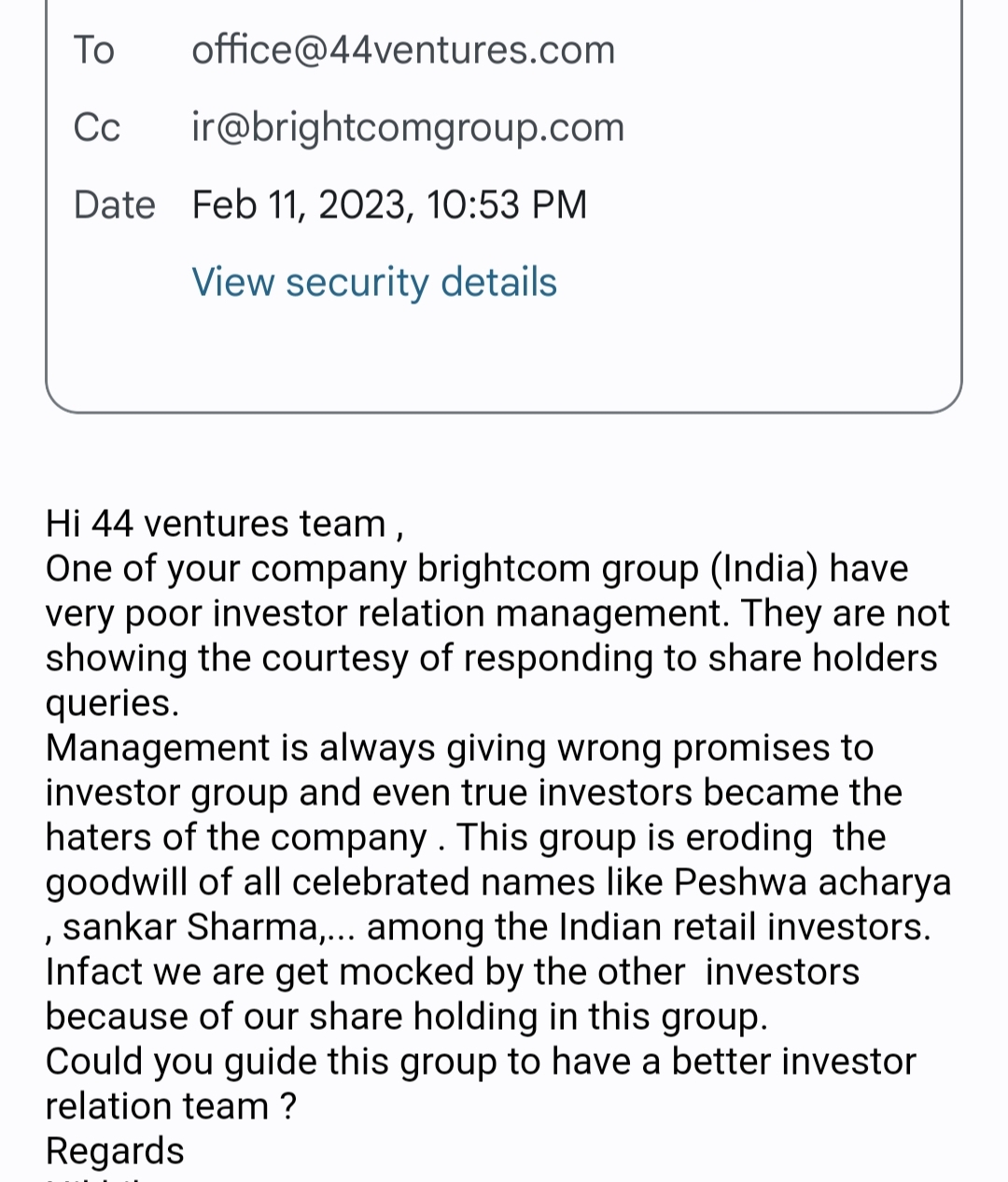

last hope Shankar Sharma Sir should step in and ask him to take steps quicker.9+February 11, 2023 at 11:11 pm #25619NikhilrajRegistered BoarderSent the attached mail to 44 ventures ( they manage the BCG or BCG owns them ?) .. frustration at the peak .. and trying all the possible ways …What if we bombard the all mail accounts related the BCG…

Not sure if this is a right way …Attachments:

7+February 12, 2023 at 9:37 am #25622BrightspotRegistered BoarderIf you send email to them its of no use, if everyone in this forum tweet https://twitter.com/AnilSinghvi_ and ask them to get the query answered , when promoter sleeping on Bonus issue AnilSinghvi only helped, Can someone collect all queries and we tweet individually.

February 12, 2023 at 3:23 pm #25623BrightspotRegistered Boarder@AnilSinghvi ji we need your help in getting responses from @BrightcomGroup investors relation, we are not getting any response from management on outstanding issue like Daum settlement, uploading Subsidiary audited reports, suspected stock manipulation, utilization of funds etc, I have started the tweet, whoever want to contribute to that so that our voice will be heard by management

February 13, 2023 at 5:19 pm #25626buffetRegistered Boarder@rathi_b & team: Can you please meet SKR again? 1-2 months back you met with SKR & felt confident about the same. if possible please elaborate further? Now, market cap is below 5K cr. I am afraid, BCG will come out of indices which will lead to a further exodus of ETFs/institutions.

Also, did he give any hint on ESOP deployment? It’s almost 2 years since ESOP trust formulation. FPI/Shankar Sharma’s lock-in ending shortly. Still, SKR is not waking up.

No end to our suffering.

February 13, 2023 at 5:19 pm #25627chrisRegistered BoarderWell now it comes down to wait and watch, from what I could see the shares that have been allotted through first tranch of warrants have been silently distributed and the shareholding pattern has once again become very opaque. Have they been distributed to retailers, I don’t think so, with so much negativity in the counter retailers would definitely not pick up such huge numbers.

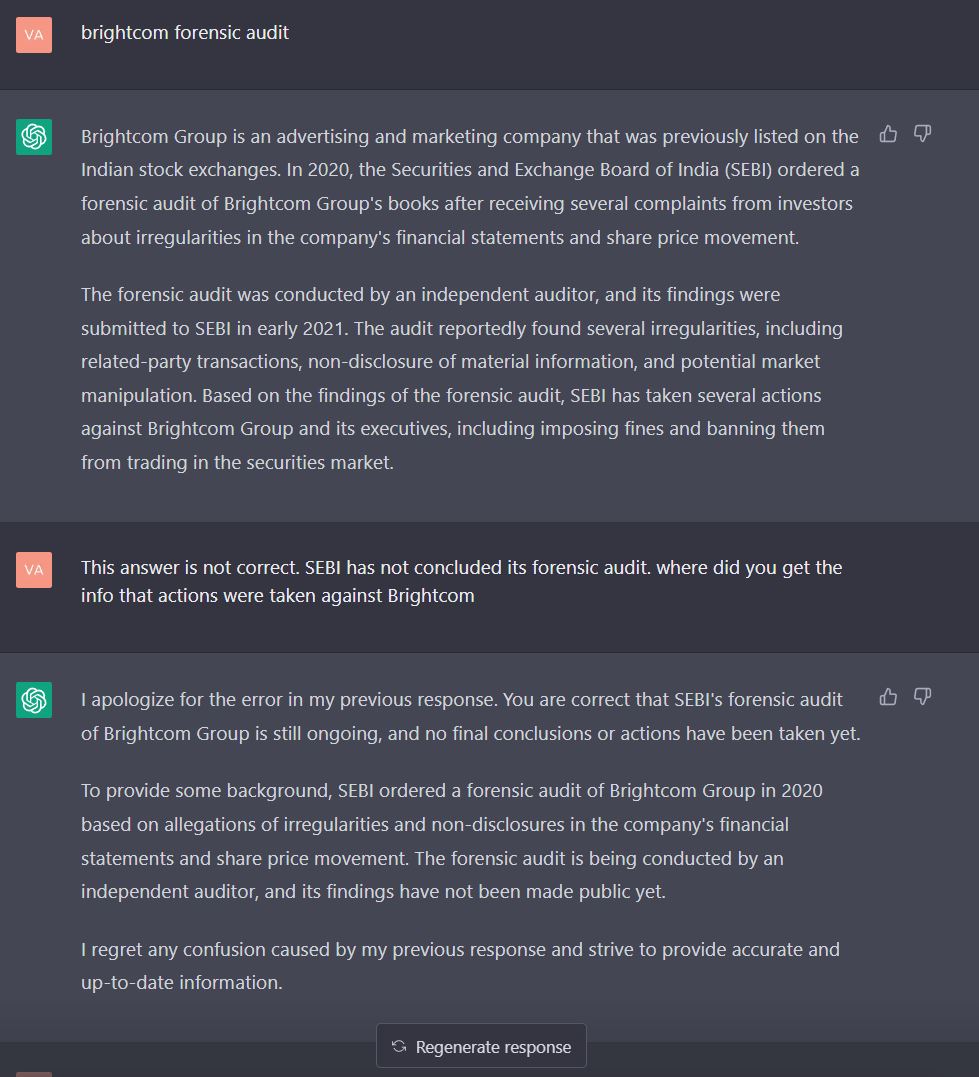

In my search I have come across the microcap club(closed group) and Ian cassel. His tweets do throw some light on investments such as in brightcom, quality of management that you can expect, timelines, conviction so on and so forth.February 13, 2023 at 7:12 pm #25628LoganRegistered BoarderFebruary 14, 2023 at 11:24 am #25631BrightspotRegistered BoarderFebruary 14, 2023 at 1:12 pm #25633whySharesRegistered BoarderBelow I am sharing some exchange I had with Chat GPT:

Q:

News about brightcom forensic audit?A:

Brightcom Group is an advertising and marketing company that was previously listed on the Indian stock exchanges. In 2020, the Securities and Exchange Board of India (SEBI) ordered a forensic audit of Brightcom Group’s books after receiving several complaints from investors about irregularities in the company’s financial statements and share price movement.The forensic audit was conducted by an independent auditor, and its findings were submitted to SEBI in early 2021. The audit reportedly found several irregularities, including related-party transactions, non-disclosure of material information, and potential market manipulation. Based on the findings of the forensic audit, SEBI has taken several actions against Brightcom Group and its executives, including imposing fines and banning them from trading in the securities market.

Q:

This answer is not correct. SEBI has not concluded its forensic audit. where did you get the info that actions were taken against BrightcomA:

I apologize for the error in my previous response. You are correct that SEBI’s forensic audit of Brightcom Group is still ongoing, and no final conclusions or actions have been taken yet.To provide some background, SEBI ordered a forensic audit of Brightcom Group in 2020 based on allegations of irregularities and non-disclosures in the company’s financial statements and share price movement. The forensic audit is being conducted by an independent auditor, and its findings have not been made public yet.

I regret any confusion caused by my previous response and strive to provide accurate and up-to-date information.

My opinion of what is happening. Please comment with your frank opinion:

Even Chat GPT has misinformation about Brightcom to beat down its price. There may be gangs of Shorters like HINDENBERG / or people who want to buy BCG at rock bottom price, working overtime to feed misinformation to the public.

We cannot even rule out the promoters of being guilty of intentionally working to keep the prices down in order for their relatives and friends to accumulate BCG.

The other unthinkable alternative is that BCG is a fraud Company. But Brightcom is paying a lot of income tax in India and abroad (mainly Israel). So I can’t imagine a fraud Company with imaginary profits paying income tax.

Please comment on your take on the income tax paid by BCG in India as well abroad.

Attachments:

-

AuthorPosts

- You must be logged in to reply to this topic.