Tagged: Mumbai Female Escorts

- This topic has 5,394 replies, 166 voices, and was last updated 2 days ago by Sobha.

-

AuthorPosts

-

June 10, 2023 at 2:18 pm #26173LoganRegistered Boarder

Some guy on Twitter posted about BCG, sharing random observations mostly about standalone numbers. The parent company (standalone) takes loan from its subsidiaries and not from banks hence the interest amount is low.

Looks like his only agenda was to find faults in the company so he forgot to check all the details properly.

If you refer Online Media Solutions’ (Israel) audited reports, you will find that the company (OMS) will not charge interest for the loans given to the parent company (BCG). This audited report was prepared and signed by EY.

On November 2019 the company signed an agreement with its Parent that effectively as March 31,2018 the company will not charge the Parent an interest for the loan.

On receivables of the parent company, the CEO said that they work with many governments and the receivable cycle there is big. Though it’ll be good if the parent company also grows and improves its business, most of the good stuff the company does is in its subsidiaries. I don’t know about others but I consider the standalone/parent company as a holding company.

Funds raised in India have been given to subsidiaries because there’s no use in keeping the funds here as all the important business is done by BCG’s subsidiaries. If they keep funds in the parent, they simply have to put it in FD or invest in some mutual fund. BCG is not a mature company to do that or the situation isn’t like there are no opportunities in the market. As everyone knows, there are plenty of opportunities in the market. Don’t forget, there are threats too like AI, privacy laws etc.

Subsidiaries have taken loan but not paid back to the parent. Well, the above points answers this also. The need for cash is in the subsidiaries as they do most of the business. It’ll be prudent to keep the money where it’s required. It’s not as if the parent company has taken any loan and gave that money to its subsidiaries. BCG is a debt free company and also all its subsidiaries are debt free.

Like he has mentioned, I’ll also mention the same. It’s your hard earned money and you should do proper research. Don’t get influenced by people seeking attention and who are biased one way. If you have any confusions then approach the management and if they don’t respond and if you feel they are not honest then approach SEBI. Don’t trust people who just look at one or two pages and act as if they know the entire history and operations of the company.

June 12, 2023 at 10:40 am #26175akkithegrtRegistered BoarderLet naysayers post whatever they want.Now, investors are not going to listen because the main doubt or investor was if the numbers were true, which the BCG has cleared by disclosing 75% audited results of subsidiaries.

I believe the worst is past for BCG, and this is the new BCG we will be looking at.Even if any penalty or unpleasant news is imposed on BCG promoters in FA (in the worst-case scenario), the business will not be affected.

So it’s time to respond to detractors who spread misleading information.June 14, 2023 at 4:25 pm #26177chrisRegistered BoarderGood evening,

Was going through the company notification on the sebi order, and the company has mentioned that this is related to a separate show cause notice received on 23/Nov/2022.

The final order of the FA, SCN still pending ?, that’s how I understand it.Opinions please.

7+June 15, 2023 at 10:52 am #26178akkithegrtRegistered Boarder@Chris ,FA’s final order is expected by the end of August.

This show cause notice is a direct rebuke to those who published an article on SRK claiming that he made a whopping 3000 crore profit by selling 10 crore shares.

I believe that a complaint should be filed by the company against the article’s publishers.

Yes, BCG has CG issues, but does it also have business issues?The answer is no.

Business is expanding, which indicates that SRk is the right man, and CG will be improved in the coming days.

There are two approaches to bcg-

1)If the business is doing well, the CG will undoubtedly improve.

2)SRK is a great businessman, but as a CEO, he needs to handle CG well, and CG will be improved in the coming days..!!June 15, 2023 at 10:33 pm #26179radhutheoptimistRegistered BoarderOfcourse this is not buy or sell call. Henceforth there will be lot of pressure both internal and external. Internally we will feel so much anxiety…. Any LCs or just a fall in price may trigger the trauma we had experienced before.

But calmly think about the fundamentals. I will consider the following points before making my decision.

– a debt free company, with substantial FCF, in a niche market, with some 30+ annual compounded growth, with projected EPS closer to 9 that barely crossed 3 PE. Is that a right price?

– Earlier LLPs were selling as if there was no tomorrow as their purchase price was in single digit. Can they do it again?

– Promotors were holding just 3% of the shares then. There wasn’t much incentive for them then had the price gone up. Is that the case now. When they are holding 18+%.

– market weren’t believing the numbers before… Now… Audited figures are available. Will the market continue to mistrust the numbers?

– FA verdict is not yet out. Whatever be the verdict…. Will it impact their business?

– what if DII starts buying… Will I get an opportunity again to purchase if I sell now?

– how exactly an investor who is very new to BCG look at the price now?

Right now I am not nervous and feel very confident. But I am not sure if I will have the same convictions if I see some LCs added with some negative news. But I know this feeling will continue for sometimes till BCG comfortably settled in the market with normal trade.

At this stage I can only keep🤞. And wait for 9am next day🥶

June 15, 2023 at 10:45 pm #26180NikhilrajRegistered BoarderRadhu ji ,

This time we have more clarity and confidence as many allegations were proved wrong and concrete proofs on existence of foreign subsidiary and their balance sheets .. So pretty confident this time ‘apna time ayega’June 16, 2023 at 11:05 am #26182NIRAJ1Registered BoarderI not received BCG shares in DEMAT ACCOUNT from last december yet by NSE.- Almost 2.5k

Anybody having same issue and solution?1+June 17, 2023 at 6:31 pm #26185chrisRegistered BoarderLot of discussion regarding Tds not payed on dividend received by BCG, was going through the income tax site and found this :

https://incometaxindia.gov.in/Pages/i-am/domestic-company.aspx?k=Dividend%20Distribution%20Tax

TDS on dividend and DDT the same or different ?3+June 21, 2023 at 10:44 pm #26188odyseeRegistered BoarderHello everyone! Are you all still around? The famed Telegram group that took the lead in all matters pertaining to BCG is now shut down as you must be aware. We are back in the game to to speak. Look forward to resuming interesting and mutually rewarding conversations and chats on new and potentially rewarding developments in relation to our favourite company and its charioteers.

Admin, trust you are still willing to steer this group and inspire some of our leading contributors, with Logan taking the pole position.

With my sincere good wishes and gratitude for the terrific inputs that so many members have provided here.June 22, 2023 at 10:15 pm #26196BBPopuriRegistered BoarderDDT Dividend distribution tax and TDS Tax deduction at source are not the same. Earlier there used to be DDT and the investor who receives dividends need not pay tax on it. Now DDT is removed and the company distributing dividends need to deduct TDS @10% when the total dividend paid in a Financial year exceeds ₹5000. We need to pay tax as per our tax slab on our total dividend income. Information on Dividend paid on 1 share is also available with ITD

4+June 22, 2023 at 10:27 pm #26200BBPopuriRegistered BoarderDuring the last financial year dividend was announced but it is yet to be paid. correct me if i am wrong. TDS was paid by the company and the information is available with the IT department for the financial years 20-21 and 21-22.

5+June 23, 2023 at 4:19 am #26201nitin_asceRegistered BoarderFYI, I checked with IR and they advised tds shall be visible in AIS by next week.

12+June 28, 2023 at 10:52 am #26204NIRAJ1Registered BoarderI added 38k today. Expecting it to reach for its full potencial…at least 30 P/E…Holding for long time.

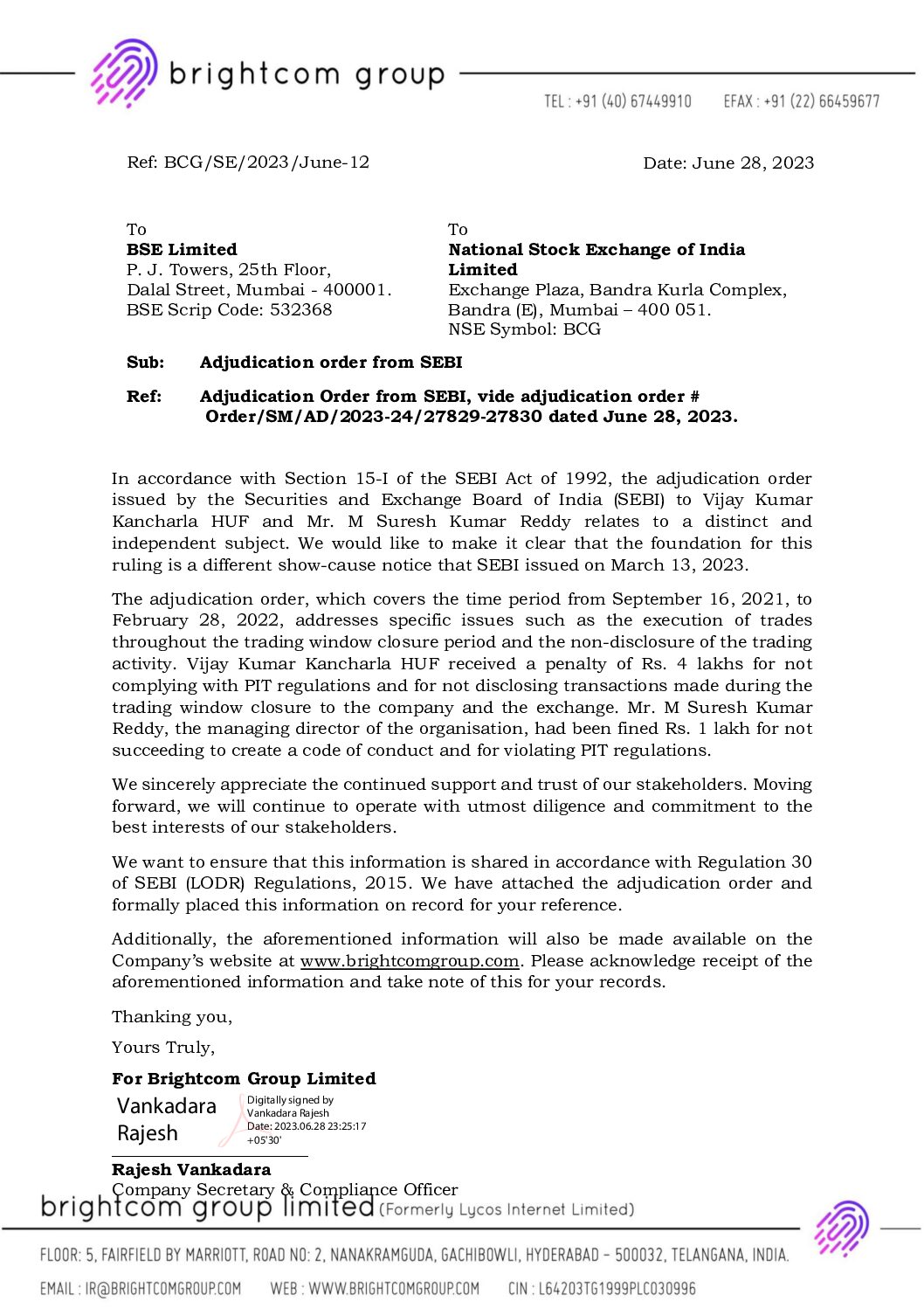

9+June 29, 2023 at 11:30 am #26206NIRAJ1Registered BoarderAnother shaw casue notice From SEBi. penalty of 4+1 lakhs to promoters

Attachments:

4+June 29, 2023 at 4:34 pm #26208Longplay55Registered BoarderDear fellow boarders,

my views are —the current adjudication order is for Sept’21 to Feb’22 period, for personal trade violations, and is separate from earlier SCN related violations. Rs=1-lak & 4-lak penalty is minor issue and importantly it’s not on BCG as an organization.

Issues are getting resolved one by one….though slow…..which is +ve for company’s image.

Also NSE indices Ltd has included BCG in NIFTY500 VALUE50 Index, effective 30th June.

Cheers for BCG’s growth prospects by coming Diwali and ahead.July 6, 2023 at 9:55 am #26213LoganRegistered BoarderCheck the latest developments happening in MediaMath company, once hailed as one of the best adtech companies, it filed for bankruptcy and owes lots of money to its creditors. Since the day I started writing in this forum, I’ve highlighted how hard surviving in this industry is and when I talked facts, some people called me paid agent, others said I write too much and that everybody should be careful about me etc. I seriously don’t understand why someone would hate anyone just because they don’t agree with them. It’s simply a waste of time to hate someone and not to concentrate on important things. I’m not someone who will highlight only the positives and give crazy targets like 100 or 1000 or 100 PE or 1000PE. I’ll talk about things which are important. Some people hated me because I supported the CEO few times (mostly on things related to business) but the thing is I’ve been more critical on him on few things (like corporate governance) than others have been but people see only the part where I supported him. Also, I didn’t and don’t blindly support the CEO on everything and will look at the whole picture before coming to conclusion.

Please read some comments made about Mediamath, adtech industry etc in few recent articles and tell me whether I was wrong anytime (past and present).

But much of the damage had already been done; Sizmek had struggled to effectively adapt to the burgeoning programmatic space in the years leading up to its acquisition and had made a handful of what adtech industry veteran Ari Paparo called “small, crappy acquisitions” of other DSPs that didn’t aid its success. In the spring of 2019, the company filed for bankruptcy – a development that rattled the digital advertising world and one that some blamed on Nguyen’s leadership.

Though Vector Capital eventually sold Sizmek for parts, with its DSP and data management business going to Zeta Global and its ad server and creative tools snapped up by Amazon, some in the industry didn’t forget Nguyen’s role in the fiasco.

“When [Nguyen was appointed CEO of MediaMath], I thought it was crazy that a struggling adtech company would go hire a CEO from the recently bankrupt Sizmek, which is one of the biggest adtech corporate disasters of our space,” says Shiv Gupta, managing partner at U of Digital, a digital marketing education firm. “History has repeated itself — [we] should have seen it coming.”

There were warning signs along the way that MediaMath may be struggling to secure the financing it needed. With no M&A action in the works, the company took out a $175m line of credit from Goldman Sachs in 2017. Then, in the spring of 2022, just three months after Nguyen’s appointment following the exit of MediaMath’s original CEO Joe Zawadski, private equity firm Searchlight Capital agreed to pump $150m into the company in exchange for a controlling stake. (Searchlight had already invested $225m into MediaMath in 2018.) Many of MediaMath’s early investors, and even Zawadski, lost their equity in the company.

“MediaMath was somewhat of a bellwether for macro trends as well as some misguided but well-intentioned decisions,” says Jeromy Sonne, an ad industry veteran and the chief executive at AI ad agency Daypart.AI. Most importantly, however, “there was a mountain of debt that was really hard to get out from under,” he says.

On the subject of fiscal responsibility, this episode underscores the harsh reality of the ad tech market. Companies must constantly adapt, differentiate themselves and secure sufficient resources to survive. Failure to do so can result in being squeezed out, as MediaMath unfortunately discovered.

The downfall of MediaMath serves as a poignant reminder of the criticality of cash flow management and credit monitoring in the ad tech industry, particularly in the face of persistent inflation and the end of easily accessible funds. As companies that previously relied on equity now turn to debt financing, it becomes imperative for ad tech businesses to showcase profitability, effectively manage risks, and embrace revenue diversification to ensure their continued success.

“Hindsight is 20/20 and it’s easy to say after the fact that their PE partner led them into a trap but, unfortunately, this is a common issue in ad tech,” said Nick Carrabia, evp at OAREX, an invoice factoring company. “Companies are blinded by valuations, cost of capital, and dilution but overlook other risks. Predatory finance partners are everywhere, make sure to read the fine print and know who you are getting into bed with.”

MediaMath missed (and dismissed) multiple opportunities to get acquired, took late-stage investments that led to a disastrous restructuring and made business bets that didn’t pan out, including that marketers would bring their programmatic media buying in house en masse.

Till now, the CEO and his team have taken mostly good business decisions (except merging with LGS). They won’t take unnecessary risks or buy something just for the sake of it or take debt (they are too conservative on debt which is a good thing but not conservative enough on equity dilution which is a bad thing). If you take loans, acquire companies just for the sake of it, and don’t worry about correct capital allocation then eventually your business will fail (like what happened with MediaMath). There were many events which would’ve resulted in BCG going the same path – like concentrating on Lycos instead of starting Brightcom programmatic advertising (Sizmek started it too late and was bankrupt later), taking on debt (LOC or other) and suffer later (especially since the last 18months where interest rates have gone up a lot). LOC terms won’t be friendly and you’d have to compromise a lot and banks get the final say and not you. Even though it took long to pay off all the debt, BCG’s team did the right thing and took a balanced approach where they didn’t let the debt harm the business.

Even now, had they acquired Mediamint or audio assets of Consumable Inc just for the sake of acquisition then it wouldn’t have worked (both valuations were based on bull market valuations). Some people were saying that only if BCG acquires any company, it will get good valuation but they don’t understand the complexities of many issues. MediaMath too acquired many companies and look where it is now? If doing only acquisition resulted in good valuation then every company would do that but is that the reality? Why did MediaMath fail even after acquiring many companies? I also agree that the way the CEO handled the communication part of the acquisitions was bad but he took a good decision in not acquiring Mediamint or audio assets for bull market valuations. What if you bought both the companies using all the cash and they failed later? Acquisition is one part but running those companies (along with your own operations) is another. To complete both the acquisitions, BCG needed more than 1250 crores and all the available cash would have to be spent on that and later to run those companies (working capital or for day to day operations) you’d again have to raise money. So you have to look at diluting your equity or take debt. Now interest rates are high and taking debt is not a good idea.

The above mentioned are one part and the other important part is the cash flow issues in the industry which is mentioned above (and mentioning again below)

On the subject of fiscal responsibility, this episode underscores the harsh reality of the ad tech market. Companies must constantly adapt, differentiate themselves and secure sufficient resources to survive. Failure to do so can result in being squeezed out, as MediaMath unfortunately discovered.

The downfall of MediaMath serves as a poignant reminder of the criticality of cash flow management and credit monitoring in the ad tech industry, particularly in the face of persistent inflation and the end of easily accessible funds. As companies that previously relied on equity now turn to debt financing, it becomes imperative for ad tech businesses to showcase profitability, effectively manage risks, and embrace revenue diversification to ensure their continued success.

When I supported the CEO and said that this is a complex industry, people rejected that and said it’s a sunrise industry and the CEO is making things up etc but did MediaMath made things up? Is it lying about its bankruptcy? Many companies went of business during 2013 to 2018-19 where they couldn’t adapt to the changes happening in the industry and mostly because of the pandemic some improved and I’ve been saying this since years. Companies must constantly adapt, differentiate themselves and secure sufficient resources to survive. This is very important in future also. That is why I always say that tech companies like BCG should never pay dividends (if they pay then pay very less amount). Paying dividend is a temporary solution which may or may not make a difference. Ultimately, if things are cleared, the company will be valued based on its business and its strengths and not on how much dividend it paid.

As investors we should look at both business and valuations. Some look only at valuation and try to bring the perception that things like Lycos, acquisitions at any price, LOC, dividends etc are more important than business. It’s true that both the valuation and business of the company are where they are because of the CEO. He took many bad decisions which harmed the valuation but he took good decisions also. MediaMath episode also shows us how important the role of CEO is. Some investors wanted the CEO to step down and the company to appoint a new CEO but that will not be a good idea, especially when your business is in this industry. CEOs should have tech mindset and should understand ground reality. For example – any other CEO would’ve concentrated more on Lycos than on the business and they wouldn’t have started programmatic advertising earlier than others and would’ve started only after it came mainstream but Mr.Reddy did the opposite. It is this type of judgment that will ensure that the business will survive.

I want to clarify my stance on acquisitions – some acquisitions made at the right time will be very useful like buying OMS etc but done at the wrong time at wrong valuations will be very bad. I’m not an expert on these things as I don’t know the ground reality and I’ll give the management the benefit of the doubt as they know what’s going on in the industry.

My request to everyone is that please don’t get influenced by both positive and negative influencers. Positive influencers will give crazy valuations and will look only at valuations and not care about the business and negative influencers too will highlight low valuations of the company and not talk about the business. Both will misguide you. Please study about the industry regularly and see how the industry is progressing, read articles, follow other companies, check their results etc. If you have doubts then approach the management and if they don’t respond then approach SEBI.

July 6, 2023 at 10:58 am #26214SaachRegistered BoarderJuly 6, 2023 at 11:23 am #26215akkithegrtRegistered BoarderJuly 6, 2023 at 3:21 pm #26216Longplay55Registered Boarder@Logan,

Please accept my sincere thanks and appreciation for your in-depth knowledge & info about ad-tech industry and BCG.

Kindly continue posting such informative articles, so that small investors like me/us can update ourselves, and get our investments in right direction. From many of your articles I understood that, you have health issues…..so I pray the All-mighty to grace you good health throughout your life span.

About SKR, your views are absolutely correct & I salute you for that. I am not a blind supporter of SKR. It is easy to give lectures on ‘how to run a business”, but in-practice, to run business worth 10000 crore turnover with 2000 cr of net profit is a herculean task. I wish all the very best to SKR and his family thru this platform.

Thanking you once again “Logan ji.”July 7, 2023 at 12:26 am #26217odyseeRegistered BoarderWhat an absolutely brilliant post @Logan. Thank you for your in-depth knowledge and insight, and your very balanced and relevant comments on the industry, and the manoeuvring and adroit ( at times not) decision making by Mr Reddy and his merry band.

One thing that starkly stands out is that this continuing growth and business development isn’t a piece of cake as we so shallowly believe when we see the quarterly results and listen to the reassuring and confident presentation by Mr Reddy and his teammates.

A tremendous amount of thought, effort and planning must be involved in the running of this complex and dynamically changing business, and to deliver the kind of results that we take for granted.

Your sobering and well studied inputs on the industry and lessons to be learned from the plight of other players in the same domain instil in us a much deeper desire to attempt to stay abreast of current happenings and developments.

Financials are relatively easier to understand; but the industry knowledge you provide all of us is truly invaluable.

My grateful thanks on behalf of all on this forum. -

AuthorPosts

- You must be logged in to reply to this topic.