Forum Replies Created

-

AuthorPosts

-

JackSparrow13Registered BoarderJackSparrow13Registered Boarder

Hi Chris,

Appreciate the sentiment.

Also appreciate the leadership of Logan during past few days.There is a simple and peaceful way of holding brightcom. Dont track brightcom news/gossips but only dividend. Brightcom has a dividend policy of distributing 15% of free cash flow. if company grows steadily, dividend will grow. and I have received dividend more than enough times to confirm, that Brightcom pays dividends.

Attachments:

JackSparrow13Registered BoarderLooks pretty ambitious and growth driven, given the frequency of switching. Started small, scaled up quickly, sought and achieved leadership positions at multiple local unlisted and listed companies. Obviously Deloitte gave him perks and prestige, but I guess too much competition for moving up even after 10 years. Took a gamble, by being a CFO of a small company (Cambridge Technology Enterprises does sales around 100 + Crores), now moving on to Brightcom, with 5k Crore sales. Definitely a big move up for him. Hope he succeeds and stays with Brightcom for long, with his growth focus.

JackSparrow13Registered BoarderIf I was a promoter, I would have ignored noise. I would focus on solely on business, and not share price. I know my share holding is bad, and share price can go from moon to mud depending on whims on shareholders, even though I have best corporate governance.

However, if i can maintain my business and dividend distributions (or buyback), that itself will provide a floor, however low that might be.

12+JackSparrow13Registered BoarderA hostile takeover would be just what the doctor ordered.

7+JackSparrow13Registered BoarderI would like to commend the optimism and maturity with which @hw_tw has moderated the discussion since yesterday. Thank you.

4+JackSparrow13Registered BoarderI really feel amazed by the promoters confidence. They run an amazing business, have single digit share holding, and are fully confident no will do a hostile takeover.

3+JackSparrow13Registered BoarderRegarding Mediamint issue, I was trying to search the reason.

Then I got this.The earlier promoter was alloted shares in April.

https://mobile.twitter.com/TusharSJadhav/status/1513859985960185863Assuming a few more “invisible” steps, i am assuming Mediamint’s results to be consolidated by September quarter (or Dec quarter at worst).

I am also very interested about when AGM will be held, and dividend credited. It was delayed last year I think. The reason is, I wonder who will pay dividend bill this year, Brightcom’s reserves or Mediamint.

JackSparrow13Registered BoarderJackSparrow13Registered Boarder“Rule Number One: Never Lose Money.

Rule Number Two: Never Forget Rule Number One”The only people I feel sad are for Index Investors. Especially, investors of a fund called Kotak Nifty Alpha 50 ETF. Nifty Alpha 50 Index, as calculated by NSE, gave Brightcom almost 10% portfolio weightage. Just imagine what will happen during next balancing in all indexes. All Index investors will lose for practically no fault of theirs.

https://www.moneycontrol.com/mutual-funds/nav/kotak-nifty-alpha-50-etf-regular-plan/MKM1409For past few months, i was studying Index funds and its varieties (My favorite is Nifty Low Volatilty). Got a good lesson from this stock price movement. Wont go below Nifty 50, in Index investing. Happy being dumb.

JackSparrow13Registered BoarderListened to the Concall. Promoter Share Holding Saga. Same old story. Do something impulsive & Smart. Then figure out how to make work legally. Similar to Bonus share issue. Very messy. Had to pay fine for this bonus delay.

For those who haven’t heard the concall, SKR very emotionally said he hadn’t sold a single share. and He was 200% committed to business. To a follow up question about share holding disclosures, he accepted there were lapses.

So, we are back to messy way of working. This mess will be cleaned in next few months. Then SKR Sir will have another outstanding idea, of increasing his and his shareholder’s misery..CFO CS issue – Didn’t work out with initial CFO candidates. Widening the net. I can understand the CFO issue. A CFO for a MNC Ad Tech company can be hard to find pedigree. My personal sense is that such a person should either be internal to Brightcom, or deputy CFO of an AdTech competitor company.

Dont really understand the delay in CS issue. There are thousands of BSE/NSE companies with CS. Delay is seriously inexplicable.

Maybe the issue is something else. Often 1st generation promoters have issue in delegating responsibilities. How much can 1 single man do ?

But still SKR has started to strengthen his team from last year. Hopefully with time, he will learn to delegate non core activities downwards. The leader of Rs.5000 Cr. Sales company should ideally be free from day-to-day mundane activities. He should spend his time searching and perceiving the next big opportunities, and preparing his company to capitalize on the same.But how can he do it, if has spend his time sending documents to BSE. Even the stupid announcement regarding publication of results in Newspapers, is being sent under his name. I truly hope, the publication was sent by his team under his name, not he himself…

Sorry, rambling post. Apologies if I have wasted your time.

JackSparrow13Registered BoarderOne the funniest criticism i have read is Q4 revenue is so less vs Q3. When learned people criticise using big issues like Daum, Bonus, acquisition, cash flow, debtor days, etc etc, and include Q3-Q4 sales comparision in the list, i feel like laughing.

6+JackSparrow13Registered Boarder^Searching for same.

2+JackSparrow13Registered BoarderThe problem with Brightcom share(not company) is very clear and has been clear since decades – low promoter shareholding. Till that gets sorted, we will have huge multi year variations in share price. My personal sense is that driven by negative environment in investing circle, we will may go back to 10 or below. This is something we need to accept, and not lose sleep over (apologies for being cynical).

What is consistently getting missed out is that business is getting stronger (fog created that subsidiaries abroad India are smoke and thin air :P). Frankly I am liking this fog. Am actually hoping more negative news/hit jobs come out. Because if the business is getting stronger, and since the company has a dividend policy, it makes sense digging in and enjoying growing dividends.(its a part of small cap investing)

Shareholding issue also seems blown out, if I take a decadal perspective (apologies). Its not that promoter shareholding has gone down to 1-2%, or drastically improved to 50%. There is hardly any special advantage that comes with promoter shareholding being 22% or 18%.

I am not really a good analyst, nor do i have any great insight on business or promoter. But I am seeing positive multi year trends in financials (repaying of debts, increase in sales, steady margins, high but steady Debtor days, slowly improving dividend payout). All that is missing is strong parentage (promoter shares)

All I am saying is if I am a long term investor, I should focus on long term. Do I see business improving ? Do I see corporate governance improving (I see no reason why, the amount of dirt directed at Twitter at SKR and Brightcom is unbelievable, and it takes a really thick skinned animal to ignore the dirt all the time)

JackSparrow13Registered BoarderHopefully, the management has had enough fun with Bonus shares, for some time.

3+JackSparrow13Registered BoarderBrightcom Mar’22 Results

My Free Opinion

What I liked –

1. Dividend Announcement – As I had posted in May 20, 2022, views of management on dividend issue, happy to see dividend improve. One of the the “old but gold” investing hearsay is a strong dividend payout, often makes helps creating a strong base for stock price.

2. Liked comparison with Apple in dividend announcement. A small hope is rising that as company grows, dividend payout would increase.

3.The management achieved their FCF commitment of Rs. 250 CR for FY’22, and has reiterated its goal of Rs. 500 cr FCF by June quarter.

4.Sounding almost opposite to above, I really liked company’s extremely vague future outlook (meaning devoid of hard financial numbers). We now live in a turbulent inflationary world. Europe is badly hit due to Ukraine war, messing up prices of everything. The last thing a logical company would want is an ambitious sounding target.

5.Letter of Intent to buy a Digital Audio Company. I think this needs a bit of celebration too.What I did not like/understand

1. Why Mediamint’s result could not be consolidated?

2.If dividend could not be now and approval taken later at AGM. Brightcom has had delayed AGMs, and this “delayed” dividend payment might again create a controversy.

3. Why FA is taking so long (of course Brightcom not to blame for this).

4.Auditing Issue, and Simplification of Subsidiaries – Less said, the betterI think this year, the management should keep their heads down, focus hard on business, not get involved in avoidable issues (like delayed/botched up bonus share listings), and try to improve their shareholding.

Looking forward to a stormy concall over promoter share holding fiasco 😉 If they dont explain it clearly in introductory remarks, will be happy to see them get a bit of plain talk… Cheers.

JackSparrow13Registered BoarderBrightcom Mar’22 Results

1. Standalone Results – Sales (Rs. 94 Cr Mar’22 vs Rs. 84 Cr Mar’21), Net Profit (Rs. 0.14 Cr Mar’22 vs Rs. 8 Cr Mar’21)

2. Consolidated Results – Sales (Rs. 1240 Cr Mar’22 vs Rs. 699 Cr Mar’21), Net Profit (Rs. 223 Cr Mar’22 vs Rs. 140 Cr Mar’21)

Full Year Ended – Sales (Rs. 5020 Cr FY’22 vs Rs. 2856 Cr FY’21), Net Profit (Rs. 912 Crs Mar’22 vs Rs. 483 Cr FY’21)

3. Vuchi Media Private Limited (Mediamint) Acquisition is yet to be completed, hence company did not consider its financials in Mar’22 Consolidated Results.

4.Brightcom has recommended a final dividend of Rs. 0.30 per equity share, subject to approval in their ensuing Annual General Meeting.

5. Management commentary on Financial Results

“The company reported a strong year, with Consolidated revenues of Rs. 5019

crores and PAT of Rs. 912.2 crores for FY22. Fourth quarter revenues were Rs.

1240 crores and PAT of Rs. 223 crores.

Consolidated revenues rising 75.8% YOY and PAT rising 88.86% YOY. Notably,

EBITDA also rose to 69.78% YOY.

Company’s Return on Equity (ROE), on an annualized basis has reached 17.23 %

approximately. We are focussed on improving this key ratio substantially.

We achieved an operating Free Cashflow of Rs 287 crores for the year FY22. We

are looking to meet the 500 crores FCF mark by the end of the June quarter.

The Board has decided to payout a significant amount of Rs.60.54 crores as

dividend, to reward its shareholders. This represents a dividend payout ratio of

around 7%, which compares extremely favorably with global tech companies,

such as Nvidia ( dividend payout ratio of around 4.5%) to Apple, which has a

dividend payout ratio of around 14%.*

• Improving Free Cash generation is a critical financial target for management.”

6.Auditing standard is same as before. Consolidating results of overseas subsidiaries. No Auditor Certificate of Stand Alone Foreign Entity included in Results.

7.As per Auditor

Standalone Result Audit (Emphasis of Matter Paragraph: 3)

SEBI ordered Forensic Audit vide Ref No – SEBI/HO/ CFID/ CFID_4/P/OW/

2021 /24343/1 dated 16/09/2021 as per the provisions and Regulation 5 of SEBI

(PFUTP) Regulations 2003 read with section 11C of SEBI Act, 1992 and Deloitte

Touche Tohmatsu India LLP has been appointed as forensic auditor w.rx.t the

financial statements for the Financial years FY 2014-15 to FY 2019-20. The said

Forensic Audit is under progress and the final outcome of the investigation is yet

to come by the time of our Certification.

Consolidated Result Audit (Emphasis of Matter Paragraph: 4)

The subsidiary company M/s. Ybrant Media Acquisition Inc has acquired M/s.

Lycos Inc.,

M/s. Ybrant Media Acquisition Inc has dispute in respect of consideration of USD

16 Million for acquisition of M/s. Lycos Inc, to Daum Global Holdings

Corporation and the district court of New York has given judgment to handover

back 56 % equity in M/s. Lycos Inc to M/s. Daum Global Holdings Corporation

and the concern matter is pending as on date.

8. Additional Matters from Management Discussion

a. The main drivers of revenue this year were:

• Overall growth of the digital marketing spend across the globe

• Agencies saw 54% year-over-year growth from 2020 to 2021. Moreover, agencies

project a whopping 68% average growth in 2022 as well.

• Improved eCPMs continue to contribute to increasing the budgets.

• Client acquisition and retention were better in 2021 than in 2020.

b. We signed a letter of Intent to acquire Digital Audio company to improve our Audio advertising footprint in the US. The Due Diligence of the same on finances and Legal side just got completed. Legal agreement work is in progress.

Outlook

We predict strong growth for the foreseeable future.

• The top two services for digital marketing companies are:

• 34% Social media marketing

• 29% Full service digital

• We feel confident, we have positioned ourselves well in the market and established our value to clients

Top challenges facing agencies in 2022 all focus on driving growth.

• 82% client acquisition

• 81% hiring

• 80% client retentionJackSparrow13Registered Boarderhttps://www.bseindia.com/xml-data/corpfiling/AttachHis/37da8ec5-dbb6-4f8f-84b3-a2cfeee3caff.pdf

The above link contains managemnet’s reply on trade receivables.https://www.bseindia.com/xml-data/corpfiling/AttachHis/a267c6e6-edea-4d53-b179-5f9589c6f8ba.pdf

Slide 7 says

The target FCF for FY22 remains at Rs 250 cr, and as stated in earlier communication, is slated to reach Rs. 500 cr by June quarter, 2022. Improving Free Cash generation is a key financial target for management.Remaining Controversy about Promoter selling share

If you need capital to grow, you often sell shares. Often promoter holding in start ups, founder led companies (1st generation) are diluted to raise shares. Even Shark Tank is just that. Let my put a reverse logic, whats the need for a promoter to run the company day-to-day, when he holds a minority shareholding. Answer – It must be passion and devotion to the company. The ultimate solution of course is a stronger promoter share.I personally dont believe management should clarify to every Tom, Dick Harry’s article, who runs 20 ratios, and eventually writes about 5 financial metrics where picture seems most disturbing (over extremely long time periods). The name Brightcom gives cheap publicity, especially if you write a article against it.

What should management do

1. Focus wholeheartedly on business. Not lose focus on every new noise maker.

2. Maintain steady dividend, and steadily imporove over years. Atleast the the “idiots” like us, who are refusing to accept “market wisdom” should be rewarded little by little.

I draw attention to management commentary about dividend (1st link).

“We are a company that has grown through acquisitions, as a result that our stand-alone parent company is relatively small, and was more in the nature of a parent company ( this is changing now, with the beefing up of standalone operations at the parent level). Our standalone revenue is at Rs 365 crore as against consolidated revenue of Rs 2855 crore, in FY 21 . Over time, we intend to increase our dividend payout, as the standalone parent starts getting to a higher size and scale. Cash generation Divergence between holding company-type parent companies and operating subsidiaries, is routinely observed worldwide, in such normal corporate structures, since most/ majority, of the business is generated at the subsidiary level and not at the parent level, for such companies”

3. Over next 5-10 years, sort out shareholding issue.I have never seen such a concentrated amount of dirt being thrown on a company. Makes me more bullish on Brightcom. But portfolio allocation is vital. Have your limit on maximum you will want to risk on a particular stock, and stick to it. We are not employees of Brightcom…

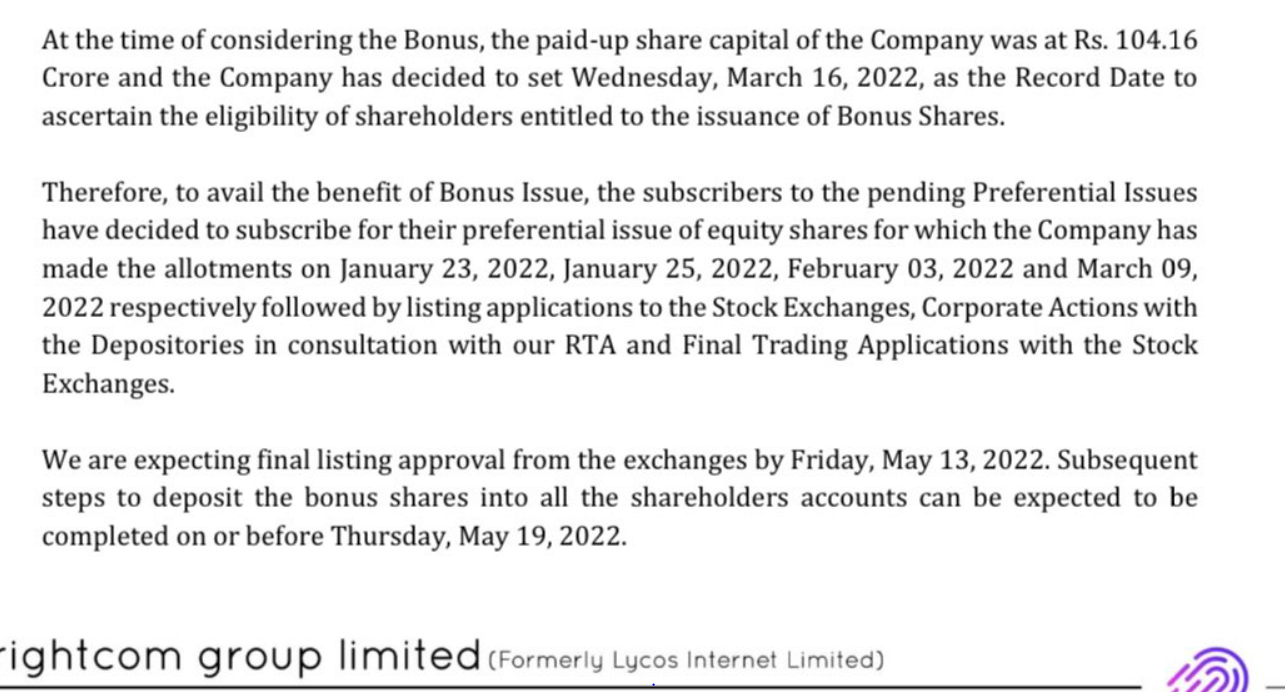

JackSparrow13Registered BoarderI did not understand this clarification at all. Really dont trust the timelines, given by management. Was this a issue of preferance shares not getting subscribed/paid, even after bonus announcement?

Attachments:

1+JackSparrow13Registered Boarder -

AuthorPosts