Forum Replies Created

-

AuthorPosts

-

NIRAJ1Registered Boarder

While refusing to interfere in an order passed by the Securities and Exchange Board of India (SEBI), the Securities Appellate Tribunal (SAT) dismissed an appeal filed by Brightcom Group Ltd (BGL) against the SEBI order.

In an order, Meera Swarup (technical member) of SAT says, “…serious allegations have been made against direct involvement of M Suresh Kumar Reddy, chairman and managing director (CMD) and SL Narayan Raju, chief financial officer (CFO) especially with regard to submission of forged or fabricated bank statements to SEBI. Though investigations are ongoing, examination of transactions pertaining to 22 allottees out of 82 allottees of preferential allotments have pointed out to evidence of prima facie diversion of funds by Mr Reddy. In the absence of any evidence to the contrary being filed by the appellants before me, I do not find any lacunae in passing of the impugned order.”

SEBI received two complaints on 6 October 2022 and 12 May 2023 about preferential allotments made by Brightcom group in the financial years (FY)19-20 and FY20-21, alleging that the company had raised money through preferential issue of shares to entities that were directly or indirectly connected to it and that the funds raised in the preferential issues were given as loans and advances to its subsidiaries.

SEBI’s preliminary findings indicated prima facie irregularities in preferential allotments by the company including circulation of funds to create the impression of receipt of funds, allotment of warrants or shares without receipt or partial receipt of funds, submission of fabricated bank statements to SEBI and significant misstatements and misrepresentation in the financial statement of the company.

SEBI, in its order, says Suresh Kumar Reddy and Narayan Raju were responsible for submitting forged and fabricated bank account statements to SEBI with an intent to mislead the investigation and cover up the irregularities. “The observations and findings clearly show the manipulations carried out by BGL and other noticees, in respect of BGL’s preferential allotments, which involve fictitious receipts of the share application money from allottees and siphoning of funds from BGL.”

However, the market regulator says BGL has brazenly attempted to cover up its misdeeds by submitting forged and fabricated bank statements to SEBI. “The blatant acts of the company and other noticees raise serious concerns about the affairs of the company and also raise doubts as to whether the financial statements prepared by the company and various disclosures made on the stock exchange platform or in annual reports in the past are correct.”

Considering the gravity of the prima facie findings, the whole-time member (WTM) arrived at the conclusion that urgent intervention by SEBI is warranted and accordingly issued a second interim order on 22 August 2023 in the matter. SEBI barred top executives of the company, as well as investor Shankar Sharma, from offloading or disposing of their shareholding in the company.

It says, “There is a real possibility that once this interim order is issued, noticees 4 to 25 may sell the shares allotted to them and make an exit. Thus, they need to be restrained from doing so. In the case of the remaining 60 allottees, suitable action would follow after the examination in respect of them is completed.”

SEBI also barred Brightcom’s CMD and CFO from holding the position of a director or a key managerial person in any listed company or its subsidiaries until further orders. Following the SEBI order, Mr Reddy and Mr Narayana Raju resigned from the Brightcom group.

Later, they challenged the SEBI order, barring them from holding any position of a director or key managerial personnel (KMP) in any listed company or its subsidiaries.

SAT, however, says, “I note that the board of directors of the Company were aware of the impending resignation of the other promoter and executive director and his ceasing to participate in board meetings from July 2023. The board was also aware of the resignation of Mr Reddy on 22 August 2023 as a consequence of the directions issued in the impugned order. However, I note that no efforts were made to appoint any executive director in the board to manage the affairs of the Company though almost four months have passed since the impugned order was issued.”

“It is made clear that any observation made by this Tribunal in this order is only prima facie and will not be utilised by either of the parties,” Ms Swarup from SAT clarified.

9+NIRAJ1Registered Boarder187 PAGE APPLICATION IS NOT AVIALBLE AS IT IS PRELIMINARY STAGE.

NIRAJ1Registered BoarderBrightcom Group Ltd has filed a fresh application before the Securities Appellate Tribunal seeking a stay on the market regulator’s order restraining ace investor Shankar Sharma and others from selling shares in the digital marketing company.

The Securities and Exchange Board of India had in August restrained Brightcom’s then chairman and managing director Suresh Kumar Reddy and chief financial officer Narayan Raju from holding directorial positions following an investigation into alleged irregularities in preferential allotment of shares.

Brightcom in its petition said the allegations made in Sebi’s order were “baseless and completely unfounded”. The company added that its turnover was expected to substantially deteriorate in the September and December quarters as a result of Sebi’s actions.

“Because of the ouster of Mr Reddy (former chairman and managing director), the company has been subjected to serious problems including the problem of its very existence,” the company said in its 187-page application to SAT. Mint has seen a copy of the petition.

SAT will hear the matter on 2 January, said a counsel aware of the developments.

Brightcom Group had first approached the appeals court on 11 December challenging the market regulator’s order. Justice Tarun Agarwala, presiding officer of SAT, refused to grant interim relief to the company after hearing an appeal earlier last week.

“We have been informed that the appellants filed an application for settlement which is pending consideration. In view of the aforesaid, we are not inclined to consider the stay application at this state,” the order said last week.

The tribunal also asked Sebi to file its reply within three weeks and posted this matter for final disposal on 9 February.

The market regulator had received complaints on 6 October 2022 and on 12 May regarding preferential allotments made by Brightcom Group in the financial years 2019-20 and 2020-21.

The complaints alleged that the company had raised money through preferential issue of shares to entities that were directly or indirectly connected to it and that the money was given as loans and advances to its subsidiaries.

They also alleged that the company did not issue proper disclosures in its annual report regarding utilisation of the proceeds of these preferential issues.

Based on Sebi’s investigation, whole-time member Ashwani Bhatia in his order restrained Reddy and Raju from holding directorial positions until further notice.

A total of 25 entities and individuals were hit by Sebi’s order.

“It is due to Sebi’s August order, the company does not have any executive director/whole-time director, and on account of such vacancy the public shareholders are suffering,” said another senior counsel involved in the matter.

Brightcom Group shares are down by nearly 34% this year, and ended trading on Tuesday on NSE at ₹19.35 apiece, down 2.5%.

BRIGHTCOM GROUP

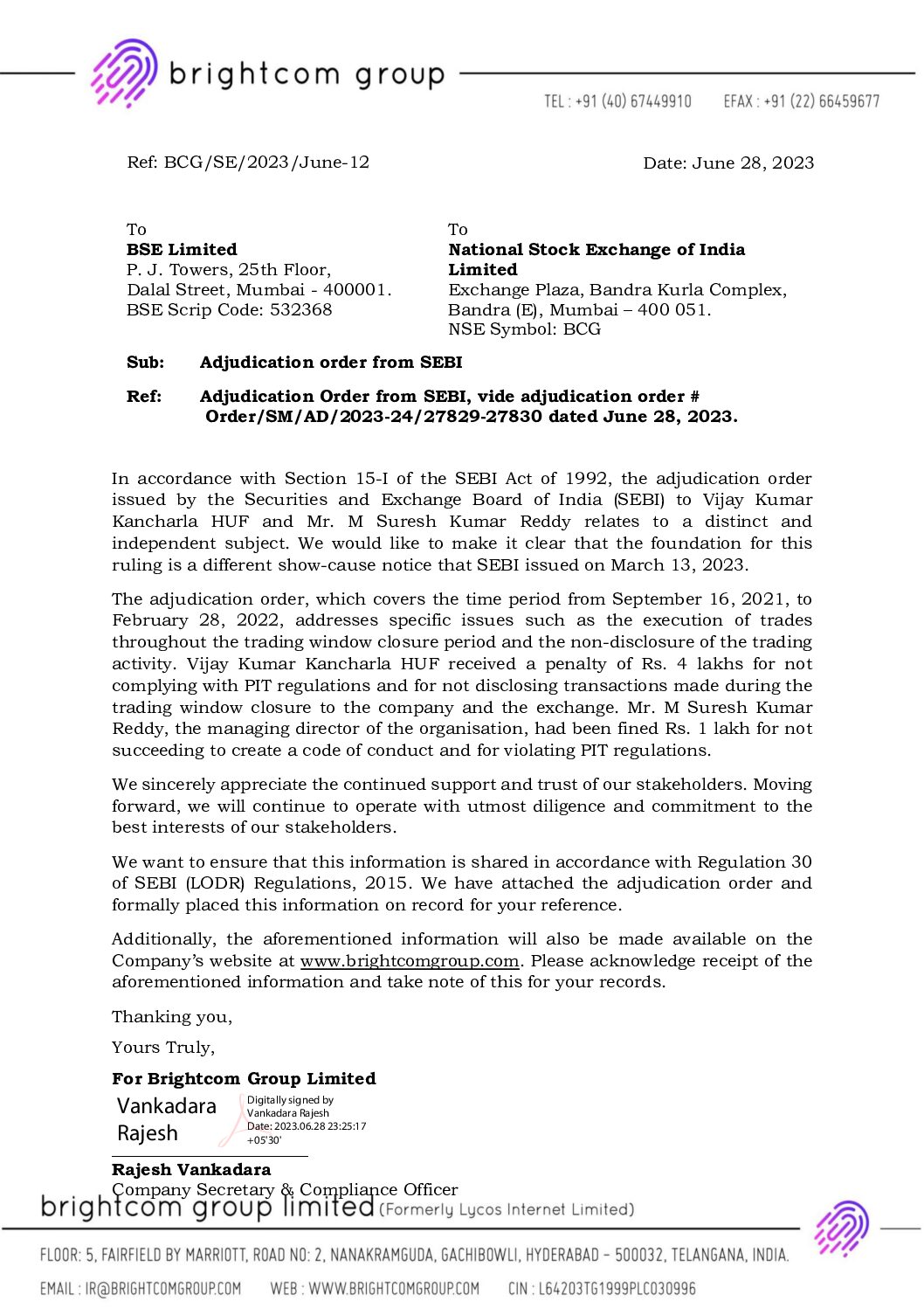

+NIRAJ1Registered BoarderAnother shaw casue notice From SEBi. penalty of 4+1 lakhs to promoters

Attachments:

4+NIRAJ1Registered BoarderI added 38k today. Expecting it to reach for its full potencial…at least 30 P/E…Holding for long time.

9+NIRAJ1Registered BoarderI not received BCG shares in DEMAT ACCOUNT from last december yet by NSE.- Almost 2.5k

Anybody having same issue and solution?1+NIRAJ1Registered Boarderadded 20k shares today.

NOW I have 1lac+ shares..7+NIRAJ1Registered BoarderI added few shares today again.

BCG will show 20%+ growth in coming year. Any thing above will be bonus.

But with all correction of problem, BCG will again reach new high in 1-2 year.

Last time I bought price of Rs 6 and hold it for 7 years and sold at 134/-

This time avarage is 15.53+NIRAJ1Registered BoarderAdded few shares today at bottom price. Holding good quantaty.

8+NIRAJ1Registered BoarderSHANKAR SHRMA’S INTERVI ON MONEYCONTROL.COM.

Part related to BCG is highlated here.How do you view Brightcom now? The regulator has raised several concerns, and the stock has crashed. How do you deal with such a situation?

My shares, till last week, have been under lock-in. I continue to hold as we speak. I will decide on my strategy as details unfold and I do not need to inform anybody about my thinking because it is my personal capital and not public funds.

The regulator has directed them to fix their compliances and reporting. That will go a long way in improving disclosures by the company. This will benefit 4 lakh shareholders of the company.

I also understand that this is a show-cause notice and the company will answer the charges. Therefore, one must not jump to hasty conclusions and must watch the developments carefully.

Like I said, I am investing my own money and am prepared for the risk. To small investors doing 4 AM investing, I have only this to say: position sizing is key and so is risk management. Do not put 50 percent of your money into a single company, irrespective of how good that company is, and, definitely, not in problematic companies which may turn out to be great investments later.What is your take on the accounting irregularities Sebi has pointed out?

The matter is sub judice, and, therefore, it is not appropriate for me to comment in detail on this. Right now, it is only a show-cause notice and the company will, in all probability, reply to these charges, with their reasons for treating impairment charges in overseas subsidiaries, in a particular manner, and not as per Indian Accounting Standards.

The nub of the matter is the treatment of impairment charges in their overseas subsidiaries.

As regards share sales by promoters, BCG has filed data on stock exchanges, which broadly state that most of the share sales between 2014 and 2020 were pledged shares being sold by various lenders, including banks, and the average price of such sales was Rs 2.7.

The company has also uploaded all the financials of its material subsidiaries on its website. Therefore, now we have far better visibility and transparency, thanks to the directions of the regulators.

I also welcome this show-cause notice because it will compel the company to strengthen its compliance standards, which will benefit all its current and future shareholders.

The market has obviously reacted very negatively to the show-cause notice and that is to be expected.

As professional investors, we must evaluate the situation with a cool mind and an analytical perspective about what the matter truly is and whether it is something which is an endgame or addressable and fixable.

That is where the difference between professional and retail investors comes in.

As a professional investor, I have seen many problematic situations over my 35 years, and, therefore, there is a huge data bank to go by, which most younger and smaller investors probably will not have.NIRAJ1Registered BoarderBRIEF INTRODUCTIONOF RAMKUMAR

Ramkumar Raja Chidambaram -I Help Businesses Unlock Growth through Strategic M&A, JV, and Divestiture Deals | 15+ years of experience as a Corporate Development Advisor for Private equity, Venture capital, and Strategic investors..HIS OPNION:

In my view, SEBI’s recent INTERIM ORDER on Brightcom Group (formerly LYCOS Internet Ltd) exposes the FRAGILITIES of accounting norms (IND AS here) and how they can get interpreted differently by different people, especially when the business is a TECH company involved in #digitalservices.Let me first tell SEBI’s allegations in Brightcom’s accounting irregularities:

[1] The 1st allegation is that the company has DELAYED THE ACCOUNTING OF IMPAIRMENT LOSSES of ~ Rs 1,000 crore (In simple words, losses were not accounted for in the years it happened but in a later period).

[2] Further, the company RECORDED THE IMPAIRMENT LOSSES BELOW THE LINE (In other comprehensive income) rather than above the line leading to misrepresentation of the profits from operations for the year when the firm recorded the impairment losses.

[3] R&D expenses were CAPITALIZED rather than EXPENSED leading to inflation in accounting profits, but it is to be noted that the assets were also inflated due to amortization.

[4] As the alleged impairment occurred in the subsidiaries, the company (operating as a holding having these subsidiaries as investments and not assets in their book) did not record losses for the investments earlier, resulting in a delay of losses.MY CONTENTION WITH SEBI OBSERVATIONS

[1] As most of the company’s investments were challenged due to GDPR (you cannot collect private data) in Europe, SEBI believes that the management should have impaired the losses from these investments in advance.MY POINT IS How can the management accurately value the impairment losses, and what if the management is confident that by tweaking its products, it complies with GDPR and no impairment is needed? Thus, the timing of impairment becomes a BUSINESS JUDGEMENT, and if management understands more about its business, it can delay the impairment until it becomes inevitable.

[2] For tech companies whose biggest INVESTMENT is either R&D/S&M/PEOPLE expenses, the accounting still asks firms to expense it rather than capitalize it, which does not give investors the real picture of a tech firm’s performance. Further’s digital companies operate in a speedy environment. Hence it becomes difficult for management to provision these impairment losses in advance compared to a traditional business.

[3] In my view, SECURITIES FRAUD happens when there is PRICE MANIPULATION, and promoters benefit when they offload their stake at that time. For CIVIL cases, the preponderance of probability, or to show that there were more alleged wrongs than not, is enough to build a case that SEBI has done.

As it is an interim order, the management can respond to SEBI’s allegations, and SEBI can retract if they find the response convincing.

However, my main contention is that IND AS accounting norms are subjective, open to interpretation, do not focus on cash flows and need business judgement on when to record impairment losses.

I hope the OUTCOME of this case helps address some of these issues.

NIRAJ1Registered BoarderDear Friends,

I started buying shares from open market. I will buy daily 5k shares till my fund gets exhusted.

I have 28k shares at average prices of 36.

Last time I hold almost 7 years with all up and downs.

After FA resports it is clear that there is no fraud and all problem can be corrected..NIRAJ1Registered Boarder1.Now SKR has to go for re-audit of BALANCe-SHeET from 2014 to 2020 as per guide line from SEBI. I suggest to appoint auditor like E&Y for all subsides and standlone level.

2.To open more for various disclosures.

3.DAUM settelment is priority to disclose audit reports of all subsidies.

4. buyback from open market.

suggession are wellcome..NIRAJ1Registered BoarderSHARE HOLDING pattern is out.

PROMOTER HAS 18.48% shares as shown in march 2022.

Lender had sold the shares in past & in 2021 which will not come back. That is why share holding decreased from 41 to 18.48%.

Promoter has aquired some shares from LLP to maintain share holding.

SKR has 0.86% with ownership of LLPs.

So there is no PUMP AND DUMP practise here.

Managment Has cleared shareholding pattern an dexplanation regarding decreased share holding.2+NIRAJ1Registered BoarderPromoter staek is 18.4%

BGl is candidate for hsotiel take over.

once lender sell shares, it will not come back.

Prmoter has to purchase from market to increase stake.8+NIRAJ1Registered BoarderBGL gave explanation for share holding.

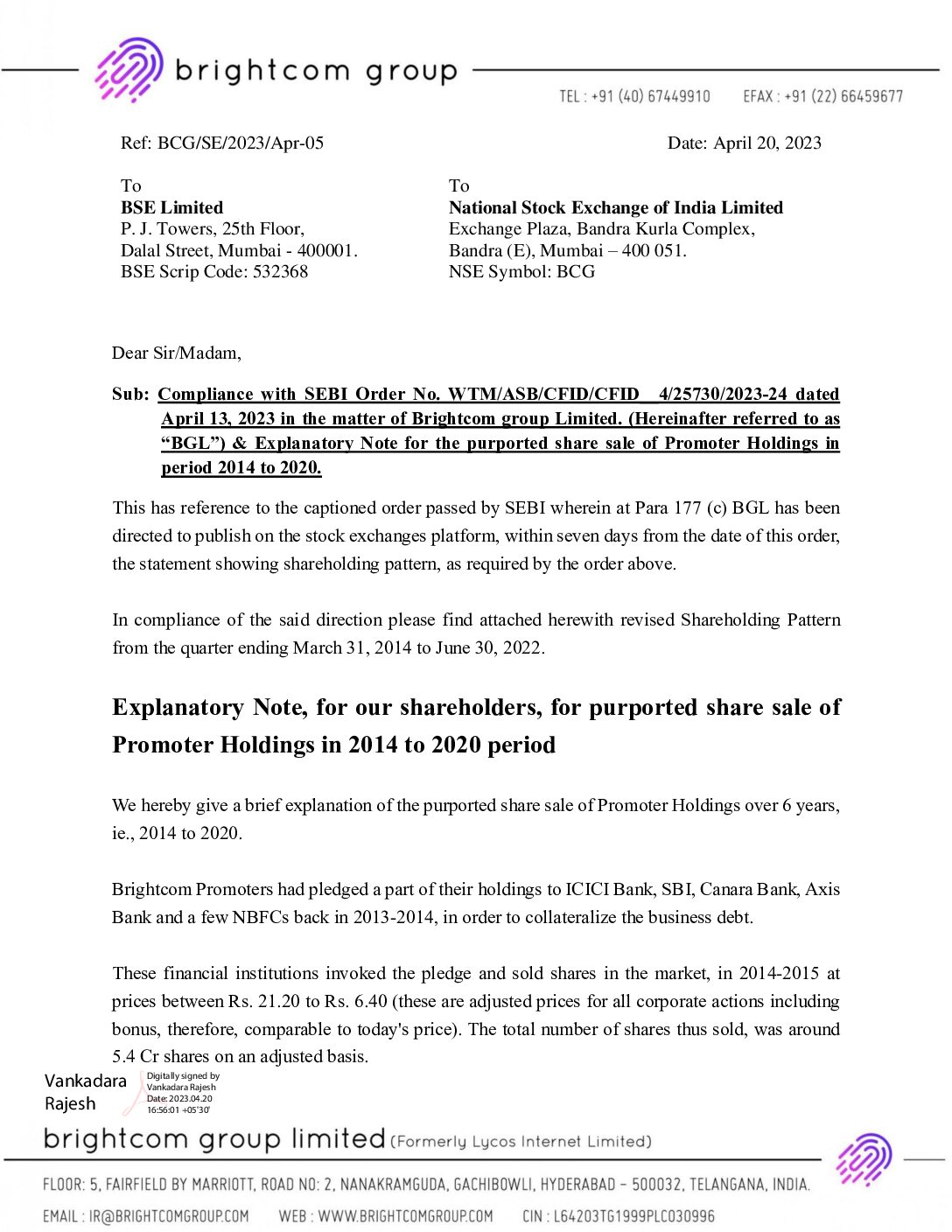

Dear Sir/Madam,

Sub: Compliance with SEBI Order No. WTM/ASB/CFID/CFID__4/25730/2023-24 dated

April 13, 2023 in the matter of Brightcom group Limited. (Hereinafter referred to as

“BGL”) & Explanatory Note for the purported share sale of Promoter Holdings in

period 2014 to 2020.

This has reference to the captioned order passed by SEBI wherein at Para 177 (c) BGL has been

directed to publish on the stock exchanges platform, within seven days from the date of this order,

the statement showing shareholding pattern, as required by the order above.

In compliance of the said direction please find attached herewith revised Shareholding Pattern

from the quarter ending March 31, 2014 to June 30, 2022.

Explanatory Note, for our shareholders, for purported share sale of

Promoter Holdings in 2014 to 2020 period

We hereby give a brief explanation of the purported share sale of Promoter Holdings over 6 years,

ie., 2014 to 2020.

Brightcom Promoters had pledged a part of their holdings to ICICI Bank, SBI, Canara Bank, Axis

Bank and a few NBFCs back in 2013-2014, in order to collateralize the business debt.

These financial institutions invoked the pledge and sold shares in the market, in 2014-2015 at

prices between Rs. 21.20 to Rs. 6.40 (these are adjusted prices for all corporate actions including

bonus, therefore, comparable to today’s price). The total number of shares thus sold, was around

5.4 Cr shares on an adjusted basis.

Thereafter, from 2016 to 2020, the Promoters had taken loans (for business purposes) by pledging

their shares to a few other private lenders, and these share pledges were also invoked and shares

were sold by these lenders, in the 4 year period.

The total number of such pledged shares sold was around 18 Cr shares (Adjusted basis). The

average price of these sales by private lenders, as calculated, was approximately Rs. 2.70/share

(Adjusted price).

Therefore, the vast majority of the promoter shares sold between 2014-2020, were neither direct nor

discretionary sales by the Promoters themselves, but, in documented fact, these shares were sold

by lenders to whom these shares had been pledged.

As is also clear from the above data, there was no enrichment by the promoters, and the shares

sold by lenders over the 6 year period, were at rock bottom prices.

Accordingly, the company and promoters shall present the above factual data, in greater and more

granular detail, to SEBI, in its upcoming submissions and hearing, and in the subsequent

adjudication process.

The company shall most humbly submit to The Regulator that there was no intention and mens rea

by the Promoters to unjustly enrich themselves & that the bulk of promoter Holding shares sold in

the 6 year period, were pledged shares being sold by lenders, and that too, at rock bottom prices.Attachments:

7+NIRAJ1Registered BoarderANOTHEER TWEET BY

Shankar SharmaAbhishek, you are absolutely entitled to say anything you wish. But, most respectfully, nobody marketed this as some “decadal opportunity”, to the best of my knowledge separately,

if you do indeed read the SCN, it says impairment charges should have been charged to PnL, hence the alleged ” overstatement “.However, all Investors disregard & look through such non recurring, non cash charges, while calculating correct PAT ( it’s called Proforma or adjusted PAT & EPS). These impairment charges were always disclosed in its balance sheet, if you see FY19-20 numbers. So not ” hidden”.

So, net worth gets written down in both cases, hence, net result is same.

(Of course , there are many lapses on compliance pointed out in SCN, all valid and must be fixed ASAP. )Lastly, as minority investors, everybody gets the exact same data, and nobody gets more information. Each investor interprets the available information through a ” glass half full” or ” glass half empty” lens.

Lastly, the Audit didn’t find anything adverse in its sales, operating ( excluding XO charges ) profit, on a global level. Just FYI.

Debate is always good in investing, in any case.

12:06 PM · Apr 17, 2023

·

I believee that all problem can be corrected and BCG will came out with bright future… Now Managment should be proactive and solve all probelm mentioned in report. I belive this not fruad but accounting mistake..NIRAJ1Registered BoarderFew comments for FA reports of BCG.

NOTE: My intension is not to save SKR or BCG’S MANAGEMENT. This is for discussion purpose.

1.AUDIT REPORTS.

.Below excerpt, taken from audit report. Main objective of accounting manipulation was to take stock price higher and dump promoters shares. This is a planned fraud of top order.

“..The accounting irregularities, due

to which the Company could paint a rosy picture of its financials, can be said

to have impacted the decision-making process for all stakeholders including

public shareholders of BGL who were oblivious to such accounting

irregularities. It is also worth noting that during the investigation period, the

promoters’ shareholding in BGL decreased from 40.45% on March 31, 2014

to 13.96% on March 31, 2020 and further to 3.51% as on June 30, 2022. The

promoters thus offloaded shares at prices which were artificially propped up

by showing higher profits through accounting irregularities.My understanding is –

BCG has done so many accounts errors/mistakes and violate SEBI’S norms.

What I understand that it is account methods that was different from SEBI’S recommended.

• Is it correctable? Yes .SEBI has ordered it.

• What is financial implication?

• Loss will be shown of around 400crs in FY 19-20 due to impairment.(450-850cr= 400) approximate.

• IF BCG has shown in every year from FY 14 TO 20, It would be average around 100cr per year.

So over all profit will be reduced by 100cr on and average. So EPS would reduced by 2 every years.

• What was price of shares from 2014 to 2020 march.?

In 2014 price was maximum 28 RS and down to 3-4 Rs in 2020.

I don’t think that promoter had pump and dump the shares at very low valuations.

• What is remedy?

To do re audit of all accounts from 2014 to 2020.

See actual profit on page no 16 of reports. They had mentioned 4 possibilities but none mentioned that BCG has made loss. Please go through that page.• All the four possibilities are given in the Table below:

Annual Consolidated figures for the financial years (INR Lakhs.)

Particulars Total Prior to 2014- 15

Investigation Period 2014-15 2015-16 2016-17 2017-18 2018-19 2019-20

Reported Profit Before Tax 52,199 60,013 61,901 59,035 60,855 61,714

Reported Profit After Tax 34,222 40,505 42,924 40,700 44,397 44,010

The FY wise break up of expenditure wrongly recognised as “Other Current Assets”: As per data Set 1 – – – – – 50,449.71 – 50,450 As per data Set 2 – – – 11,533.79 14,003.37 25,015.87 – 50,553 As per data Set 3 In absence of detailed breakup, individual mapping of the impaired asset could not be carried with the recognised assets and hence it could not be ascertained in which year the impaired assets were initially recognised.

As per data Set 4 1,964.74 11,399.78 7,010.24 12,208.81 8,037.69 9,007.69 1,065.93 50,695 Profit Before Tax if correct accounting treatment was followed:

Data set 1 52,199.00 60,013.00 61,901.00 59,035.00 10,405.29 61,714.00

Data set 2 52,199.00 60,013.00 50,367.21 45,031.63 35,839.13 61,714.00

Data set 3 Not Ascertainable

Data set 4 40,799.22 53,002.76 49,692.19 50,997.31 51,847.31 60,648.07Profit After Tax if correct (Ignoring Taxation impact)

accounting treatment was followed:

Data set 1 34,222.00 40,505.00 42,924.00 40,700.00 -6,052.71 44,010.00

Data set 2 34,222.00 40,505.00 31,390.21 26,696.63 19,381.13 44,010.00

Data set 3 Not Ascertainable

Data set 4 22,822.22 33,494.76 30,715.19 32,662.31 35,389.31 42,944.072. About Share holding patterns

I don’t have any explanation of reduction of share from 41% to 33%

Company had diluted share holding from 33% to 18% due to preferential allotment.

Company has pledged or transfer shares from promoter to pledge company off market. That is foolish step. Price of shares was RS 3-4 in march 2020. Pledged company had sold in open market later on. Now SEBI has given clear cut guide lines. SKR cannot do much unless he purchased shares from open market from money he got for pledging/ transfer.3. DISCLOSURE:

Management is very poor in disclosure and we repeated said in conference. SEBI has taken this point very seriously. They should fine them. Like results from FY 2014 TO 2020.

4. NEW AUDITOR

BCG should appoint new auditor like E&Y.

Once everything get cleared BCG will show it full potential. I could find money manipulation or Fraud in any reports.NIRAJ PARIKH

16+NIRAJ1Registered BoarderBCG is now take over candidate. I discuss few big investor to corner free float up to 60%. Let us see what happen in future..

NIRAJ1Registered Boarderconcall summary : source from a group : i am just sharing it here… 1- Gratitude for staying with company and wishing a prosperous new year.

Raju CFO speaks- FA- replied to regulatory authorities. 6 yrs and all subsidiaries. Unique business model. Annulment process in way. No cash paid to MM. All are consolidated companies are AUDITED. Each subsidiary is audited. Israel subsidiary by E & Y. Company not involved with 5th & 6th trades.

Satish Speaks- Audio acquisition. All due process adhered to. Update in February.

Peshwa speaks- Discussion going on weekly basis. SBLC from bank. Paperwork is being done. Will be finished soon. Quantum Computing in process. for all queries. Trying to establish more robust mechanism.

Shareprice- company has performed very well. More than 40% growth. Results sooner this time. Outstanding issues are taking long time. We take responsibility for informing early some things which are jow taking time. It will shine brightly in 2023. Market will recognize us soon.

Vaibhav- Suggestion to hire independent auditor to audit and give report. Answer- will evaluate. Daum once done we will upload audited results. Pledging of shares to appear back in promoter holding. We are fighting back to get back shares. The people who have sold it will have to buy it from the open market and give. Q4 DII meeting..

Raju and Peshwa- concentrated strategy to get them on board. Each of FII & DII have their own strategy. ESOP trust may buy. Funds are raised to grow the company.

Intent IQ patnership – no answer. Its mainly in Israel. The collaboration will help us monetize a lot of traffic. Why Equity dilution was done at so low rates. We wanted to be a debt free company. Positive free cash flow company. Strategic decision to stay out of debt. Will play out well longterm. Better that debt companies are debt free.

Promoter shareholding- before Match was 24% portion was pledged which was transferred off market. So it was reported as not being Promoter. Pledged shares- trying to get back. Same old answers being given… We are aware that shareholders are suffering in spite if company doing well. Few reasons that are there will be resolved. Long term vision- We are in an excellent field of business. Evolving business and we have to be nimble enough.

Abroad listing- will look at it when the markets are conducive. We will make a few deals with the 5G players.

Closing comments- Grateful for opportunity. Our dream is to revolutionize digital marketing. In 25 countries. Future- will bank on your support. Prirotized building sustainable business model. Not worried by short term. -

AuthorPosts