Tagged: Call Girl Rishikesh

- This topic has 5,566 replies, 167 voices, and was last updated 2 weeks, 2 days ago by Logan.

-

AuthorPosts

-

April 29, 2023 at 11:44 am #26014SaachRegistered Boarder

@akkithegrt, well very strong and straightforward views and belief, appreciate. Only my small question to understand so as to apply this technic, how to know and decide the peak level? warmest regards.

April 29, 2023 at 1:04 pm #26015akkithegrtRegistered BoarderApril 29, 2023 at 2:47 pm #26016Longplay55Registered BoarderApril 29, 2023 at 7:09 pm #26017NikhilrajRegistered BoarderAs of now all the very recent developments are favourable for the investor community. Whether market will immediately reward this , nobody knows . Still there are many reasons to restart the dreams which had paused or even turned nightmares …

Let’s hope company will fullfill all its promises before the next concallMay 1, 2023 at 11:42 am #26018NIRAJ1Registered BoarderBRIEF INTRODUCTIONOF RAMKUMAR

Ramkumar Raja Chidambaram -I Help Businesses Unlock Growth through Strategic M&A, JV, and Divestiture Deals | 15+ years of experience as a Corporate Development Advisor for Private equity, Venture capital, and Strategic investors..HIS OPNION:

In my view, SEBI’s recent INTERIM ORDER on Brightcom Group (formerly LYCOS Internet Ltd) exposes the FRAGILITIES of accounting norms (IND AS here) and how they can get interpreted differently by different people, especially when the business is a TECH company involved in #digitalservices.Let me first tell SEBI’s allegations in Brightcom’s accounting irregularities:

[1] The 1st allegation is that the company has DELAYED THE ACCOUNTING OF IMPAIRMENT LOSSES of ~ Rs 1,000 crore (In simple words, losses were not accounted for in the years it happened but in a later period).

[2] Further, the company RECORDED THE IMPAIRMENT LOSSES BELOW THE LINE (In other comprehensive income) rather than above the line leading to misrepresentation of the profits from operations for the year when the firm recorded the impairment losses.

[3] R&D expenses were CAPITALIZED rather than EXPENSED leading to inflation in accounting profits, but it is to be noted that the assets were also inflated due to amortization.

[4] As the alleged impairment occurred in the subsidiaries, the company (operating as a holding having these subsidiaries as investments and not assets in their book) did not record losses for the investments earlier, resulting in a delay of losses.MY CONTENTION WITH SEBI OBSERVATIONS

[1] As most of the company’s investments were challenged due to GDPR (you cannot collect private data) in Europe, SEBI believes that the management should have impaired the losses from these investments in advance.MY POINT IS How can the management accurately value the impairment losses, and what if the management is confident that by tweaking its products, it complies with GDPR and no impairment is needed? Thus, the timing of impairment becomes a BUSINESS JUDGEMENT, and if management understands more about its business, it can delay the impairment until it becomes inevitable.

[2] For tech companies whose biggest INVESTMENT is either R&D/S&M/PEOPLE expenses, the accounting still asks firms to expense it rather than capitalize it, which does not give investors the real picture of a tech firm’s performance. Further’s digital companies operate in a speedy environment. Hence it becomes difficult for management to provision these impairment losses in advance compared to a traditional business.

[3] In my view, SECURITIES FRAUD happens when there is PRICE MANIPULATION, and promoters benefit when they offload their stake at that time. For CIVIL cases, the preponderance of probability, or to show that there were more alleged wrongs than not, is enough to build a case that SEBI has done.

As it is an interim order, the management can respond to SEBI’s allegations, and SEBI can retract if they find the response convincing.

However, my main contention is that IND AS accounting norms are subjective, open to interpretation, do not focus on cash flows and need business judgement on when to record impairment losses.

I hope the OUTCOME of this case helps address some of these issues.

May 1, 2023 at 6:29 pm #26019NIRAJ1Registered BoarderSHANKAR SHRMA’S INTERVI ON MONEYCONTROL.COM.

Part related to BCG is highlated here.How do you view Brightcom now? The regulator has raised several concerns, and the stock has crashed. How do you deal with such a situation?

My shares, till last week, have been under lock-in. I continue to hold as we speak. I will decide on my strategy as details unfold and I do not need to inform anybody about my thinking because it is my personal capital and not public funds.

The regulator has directed them to fix their compliances and reporting. That will go a long way in improving disclosures by the company. This will benefit 4 lakh shareholders of the company.

I also understand that this is a show-cause notice and the company will answer the charges. Therefore, one must not jump to hasty conclusions and must watch the developments carefully.

Like I said, I am investing my own money and am prepared for the risk. To small investors doing 4 AM investing, I have only this to say: position sizing is key and so is risk management. Do not put 50 percent of your money into a single company, irrespective of how good that company is, and, definitely, not in problematic companies which may turn out to be great investments later.What is your take on the accounting irregularities Sebi has pointed out?

The matter is sub judice, and, therefore, it is not appropriate for me to comment in detail on this. Right now, it is only a show-cause notice and the company will, in all probability, reply to these charges, with their reasons for treating impairment charges in overseas subsidiaries, in a particular manner, and not as per Indian Accounting Standards.

The nub of the matter is the treatment of impairment charges in their overseas subsidiaries.

As regards share sales by promoters, BCG has filed data on stock exchanges, which broadly state that most of the share sales between 2014 and 2020 were pledged shares being sold by various lenders, including banks, and the average price of such sales was Rs 2.7.

The company has also uploaded all the financials of its material subsidiaries on its website. Therefore, now we have far better visibility and transparency, thanks to the directions of the regulators.

I also welcome this show-cause notice because it will compel the company to strengthen its compliance standards, which will benefit all its current and future shareholders.

The market has obviously reacted very negatively to the show-cause notice and that is to be expected.

As professional investors, we must evaluate the situation with a cool mind and an analytical perspective about what the matter truly is and whether it is something which is an endgame or addressable and fixable.

That is where the difference between professional and retail investors comes in.

As a professional investor, I have seen many problematic situations over my 35 years, and, therefore, there is a huge data bank to go by, which most younger and smaller investors probably will not have.May 2, 2023 at 11:40 am #26020akkithegrtRegistered BoarderAffle’s corporate governance may be best but look at BCG’s financial numbers. Even if say 75% of financial numbers are true, revenue comes around 5000–6000 crore. At least it should trade at a valuation of 10,000 CR until all points are clear.

SEBI has given BCG’s management a chance to clear the mess, which does not have an impact on business.

The business is doing great. The only thing now is that management should be transparent with shareholders.

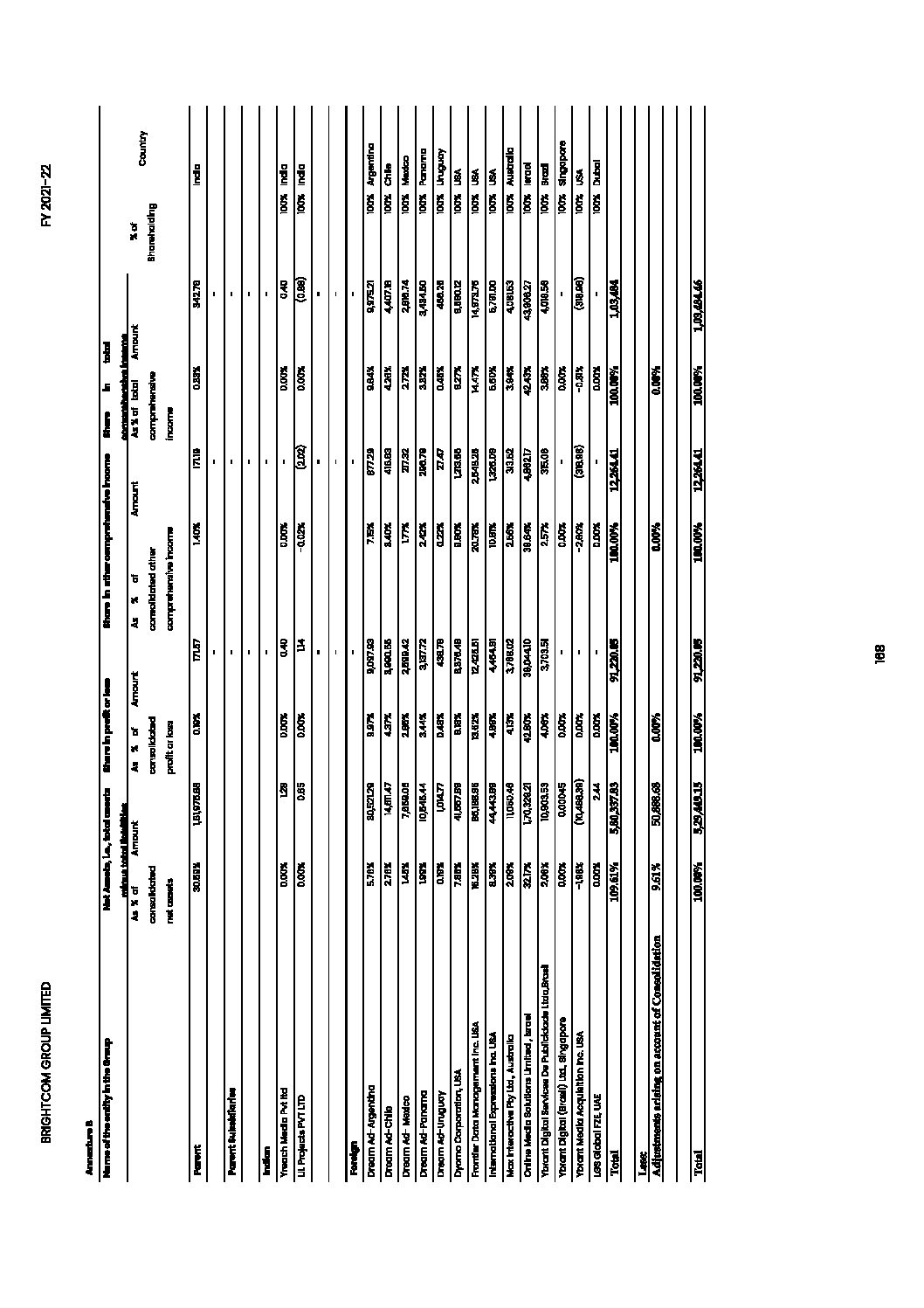

May 5, 2023 at 3:53 pm #26029vstvmRegistered BoarderAll the subsidiaries financial statements for the period 2021-22 are uploaded in BCG website. (attached herewith)

Also the volume for the recent days indicates it will move forward.

Sr. boarders please throw some input, as the board is very silent for few days.Attachments:

8+May 5, 2023 at 7:30 pm #26031whySharesRegistered BoarderHere is my take on SRK’s journey to the making of BCG what it is today. It is pure educated guess work and what I imagine may have happened.

The evolution of BCG from being an online Greeting Card Company to one of the world’s leading programmatic digital Ad-Tech Company is something spectacular. SRK did it by taking over budding Ad-Tech Companies from all the world. In the process Mr. SRK borrowed left and right and pledged whatever shares he had. His single minded drive and vision to grow BCG into the new 4AM field of Ad-Tech taking big risks with his personal fortune has to admired. In between his pledged shares got sold, he may have been on the verge of Bankruptcy and about to lose all what he worked for.

Anyone in this position would have resorted to wheeling and dealing, sometimes at the borders of legality. To regain control of his Company he may have resorted to desperate means like issuing preferential shares, unwanted bonuses, not declaring share holdings, announcements of taking over Companies like Media Mint, Audio Company, etc. etc. – all done for survival.

Now I think he is firmly in the driver’s seat and BCG should be rising to new highs.

Here is a factual listing of BCG’s History

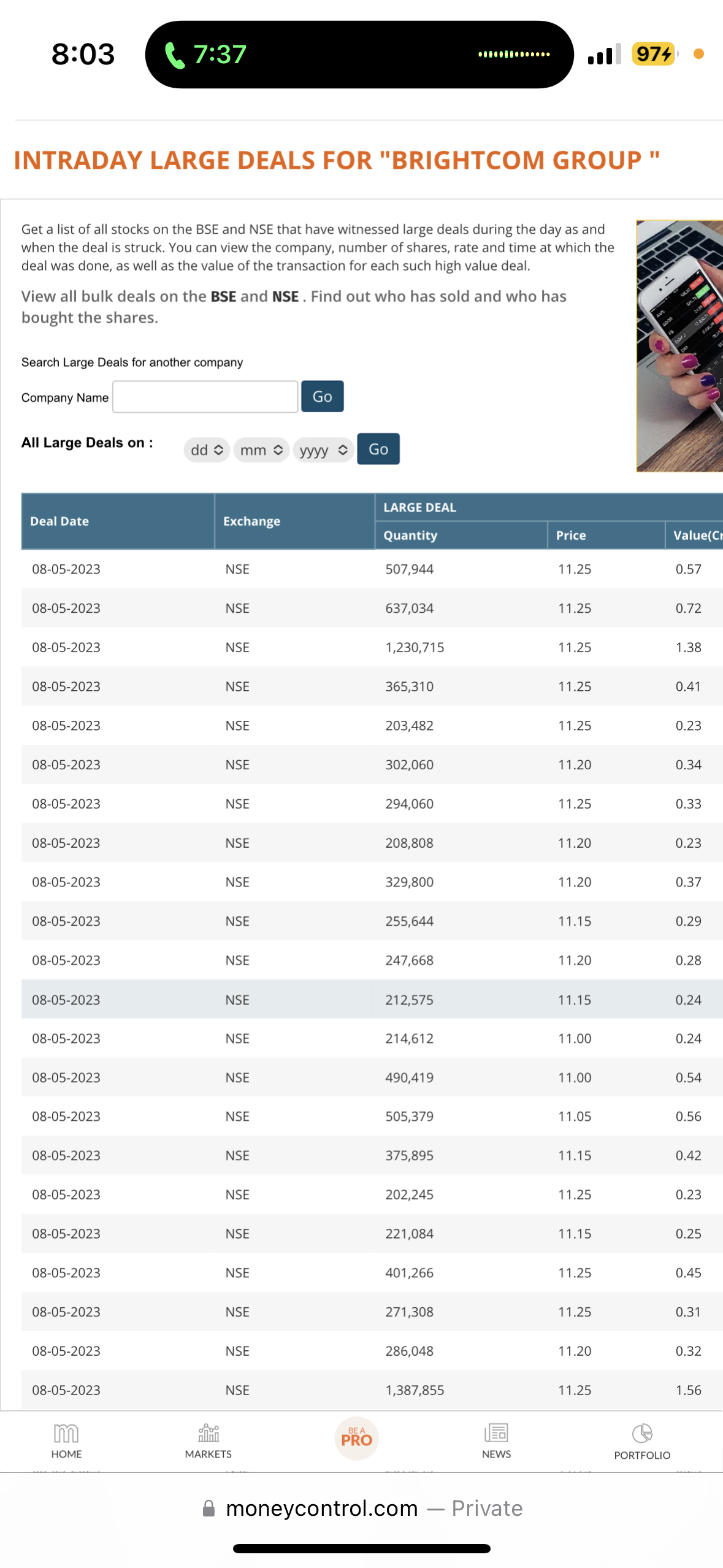

https://www.moneycontrol.com/company-facts/ybrantdigital/history/LGSMay 8, 2023 at 8:04 am #26034chrisRegistered Boarderhttps://www.moneycontrol.com/stocks/marketstats/blockdeals/view_deals.php?sc_did=LGS

Already showing deals on the eighth of May ?

Attachments:

3+May 8, 2023 at 8:56 pm #26038Rising SunRegistered BoarderOnly thing which can lift market sentiment is over 250 crores buyback.

The management claimed last year that the Company is able to generate 250 crores of free cash flow every quarter.

This year, with increase in sales the free cash flow is expected to increase.

With no acquisitions planned, the management should consider open market buy back of a huge amount. Anything less than 250 crores will be like peanuts. Like how they announced 5 crores dividend.

The management has claimed cash balance of more than 1200 crores at December end, which after the most busy season and highest amount of Debtors. They said, they will have very high cash flow this quarter (as it would be cash flow of Q3 + Q4).

Investors want to know:

1) Where is the money?

All big talks are a waste, if they cannot show the money.

2) Who is doing the audit of Brightcom Books?

Given that the current auditor is hand in glove with management of making money (46 lakh shares alloted to them must have been sold long time back).

Whatever SEBI has done is right. As there are clear indications of indirect insider trading.

6+May 8, 2023 at 9:06 pm #26039Rising SunRegistered BoarderThe average buying price of lakhs of investors is more than 40, 50, and many cases 60 and 80.

As everyone knows, the number of retail investors increased from 1 lakh to 4 lakhs.

Hence the feeling of being cheated, as all the close associates of management (LLP’s) have sold.

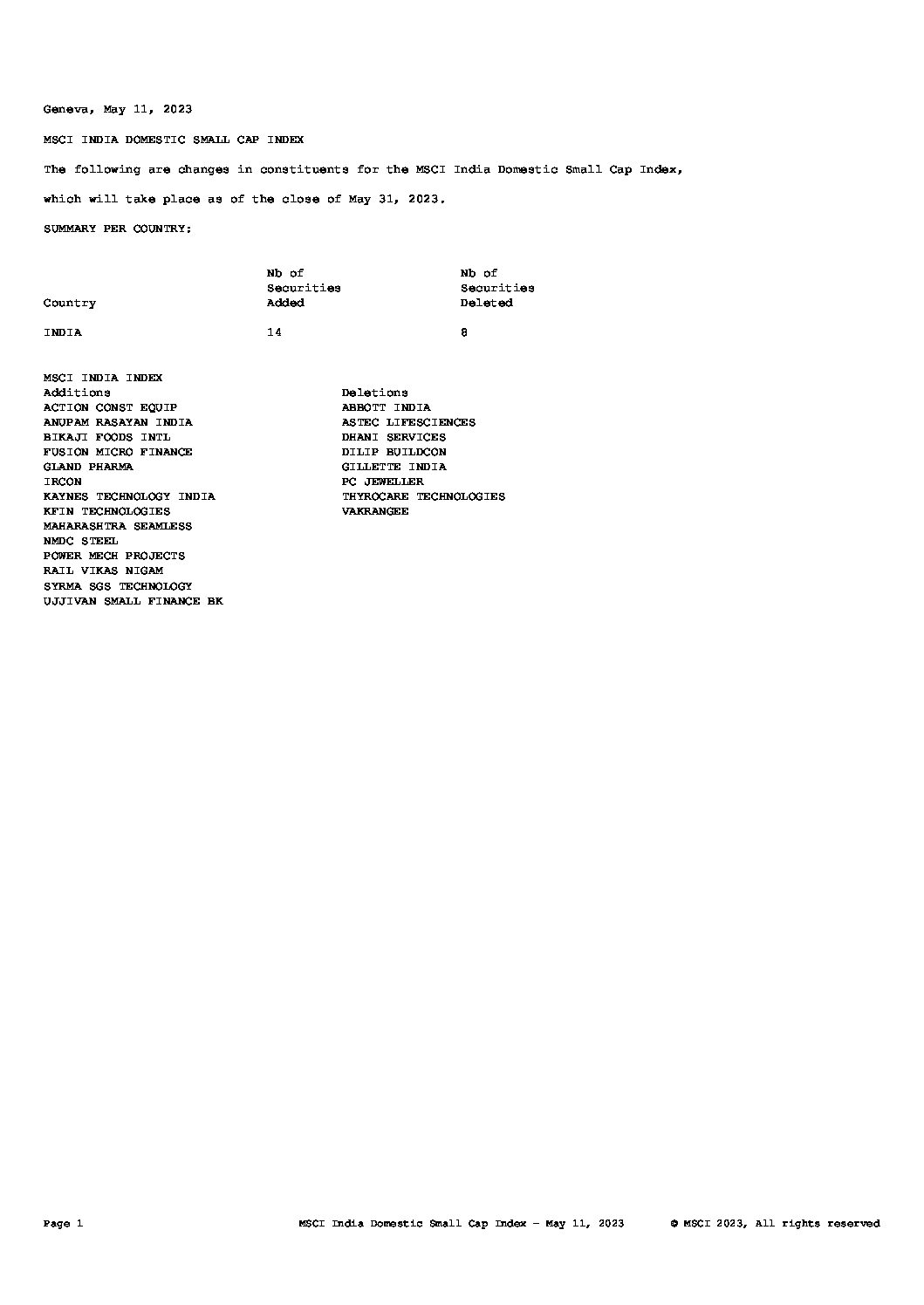

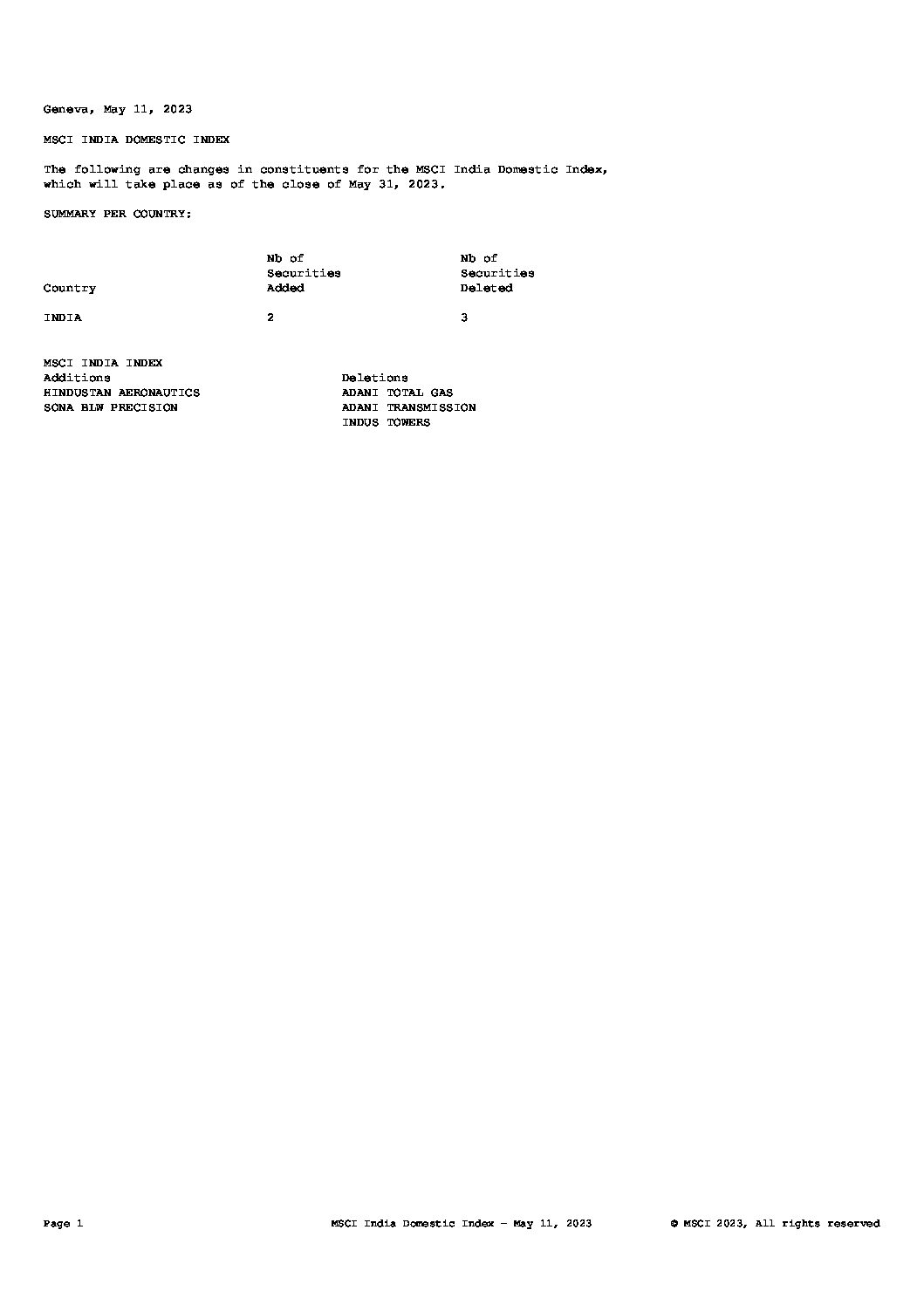

9+May 12, 2023 at 7:55 pm #26046vstvmRegistered BoarderMSCI Index review for May 2023 is released and BCG is still retained in the list.

Hope they are aware of the interim SCN from SEBI.

Wish to see excellent volumes with new ATH with the grace of god.

MSCI report attached.11+May 14, 2023 at 6:51 pm #26052akkithegrtRegistered BoarderQuarter 4 results will be good for BCG. This will further strengthen the rally. If BCG closes the remaining NC’s on time as per Sebi’s requirement, this will further increase shareholder’s confidence.

If all goes fine, then 2023-2024 may be one of the best years for BCG’s shareholders.

Hope for the best…!!!

May 21, 2023 at 2:44 am #26059LoganRegistered BoarderI’d be more happy if BCG doesn’t pay any dividend and instead use all the cash available to grow the business and become stronger. In the world of AI, ChatGPT, CTV, Quantum Computing (which will become big just in few years) etc, it’ll be prudent if tech companies like BCG look at stability and growth more than paying dividends (obviously I’m not forcing my views on others).

Some people say that the company should pay most of its profits as dividends and only then the management is serious etc, but this point doesn’t make sense for tech companies. If people invest in tech companies thinking they’d be paid more dividends like how typical IT companies pay (which are mostly IT service companies) then they are wrong as most tech companies and all ad-tech companies don’t pay dividends.

This year there’ll be a recession in the US and next year there’s the US presidential elections. One will be about how you tackle problems when there’s slowdown, and the other will be about growth. It’s good that BCG is a debt free company with no baggage (debt wise not governance wise). Companies which have borrowed more will find it tough in the coming months/years. There’ll be a credit crunch because of which it’ll be hard to raise money either through debt or equity. You will survive and you can take advantage if you have enough liquidity.

Let me share some interesting points. I’m guessing BCG has $100-150M cash (as per Q2 results) whereas Google has $100-150B cash (1000 times more i.e. if BCG has 1 rupee then Google has 1000 rupees). Amazon has more than $80B, Facebook has $40-50B, Microsoft has more than $100B, and Apple has more than $50B. All these are big in ad-tech and growing. Recently Amazon, Microsoft and Apple are concentrating more on advertising. Apple actually implemented strict privacy rules but it started its own DSP (demand side platform). And TTD has $1.5B in cash (10 times more than BCG).

When you are competing with giants who are flush with cash, you need to be innovative and have sharp focus, else you’ll find it difficult to survive.

Next year’s USA election will be very interesting. They’ll spend more ads and regional news publishers (B-local) will get more traffic and there’ll be more podcasts which would benefit Consumable Inc.

If the CEO/management maintained good image and if the corporate governance was good then the market would’ve considered the positives of BCG but the CEO, who is solely responsible for the pathetic state of governance, doesn’t care about valuation and how shareholders and the market think. Had he and the other promoters disclosed their actual holdings and if they explained the shp issue before itself, the stock wouldn’t have crashed like this. And because of his decision to give shares to selfish traders who became rich at the expense of retail shareholders, the stock wouldn’t have traded at these levels. No shareholder would’ve objected if the CEO took crores of salary and paid off his debts and got his shares unpledged.

He always gets annoyed and irritated if any shareholder talked about SHP issue but it was his duty to disclose that information which he failed to do so which created so much confusion and it took SEBI’s order for him to disclose that. I’m not sure we’d have got any info if SEBI didn’t force them to disclose. We should thank SEBI for that.

According to me, if they improve governance, comply with all the rules and regulations and communicate well (tell truth instead of giving same old reasons) then the market will give a good valuation to the company.

Once any company starts paying dividends and if they stop later then obviously it’ll look bad so I’m okay with them paying whatever they think is right but I don’t want them to pay more just for the sake of it. If they don’t find any opportunity then they can pay more but like I’ve mentioned above, there are many opportunities and it’ll be better if they use the cash for growth purposes. Let them start looking at potential acquisitions or JVs.

May 21, 2023 at 12:39 pm #26060NikhilrajRegistered BoarderLogan Sir ,

Agree with your point. if company use the money for growth opportunities than paying dividend it is really good thing . But in the cuttent scenario , investors don’t have clarity to belive company is utilising the money they raised so far for the growth . Acquisitions were cancelled or turner to JVs with zero investment. Unless company give a clear picture on it’s future plans, dividends,buybacks are the reasons to cheer for retailers .. May dividends create a image that the company is investor friendly and their profit claims are genuine .May 21, 2023 at 5:22 pm #26061LoganRegistered Boarder@Nikhil Raj, stock price or the valuation are at these levels because of 4 things – one is FA, second is SHP issue, third is corporate governance (which includes many things like not communicating well with shareholders, not appointing a CS even after one year after the previous CS quit, not appointing CFO quickly, taking too much time to give bonus shares, taking years to close DAUM issue and not informing sooner that acquisition plans changed and took long to reveal the change of plans) and finally the fourth which is the most important thing which created so much supply is issuing shares to selfish traders who made hundreds of crores at the expense of retail investors.

Also, business related, SEBI’s investigation didn’t find anything wrong in the company’s operations or didn’t find any misuse or siphoning of funds but it concentrated more on how the impairment was reported. Recently SEBI did forensic audits on a few companies and it found those companies showed fake revenues – Securekloud and Seya Industries.

The company has used the funds well to grow the business. Me and all the shareholders would’ve been worried if SEBI found issues in the business. Also, they’ve uploaded audited results of major subsidiaries so now the market will start trusting the numbers than it did when everything was unclear.

I’m not saying that the company should stop paying dividends but what I’m saying is that let them not give more dividends and miss out on the opportunities that are there in the market (both organic and inorganic and it doesn’t have to be only inorganic). As far as I know, shareholders and the market will be happy if all the issues are fixed and if the company improves governance than if the company pays dividends or buys back shares.

I’m not supporting the CEO but I kind of get why he and the management changed their plans. Both Mediamint and audio ad plans were made when there was a bull market. Mediamint is a backend service company and you can manage backend by hiring engineers (huge supply is there on that front) and train them for months. You can get it done for way way less than what they agreed to pay Mediamint. Audio ad part, with Consumable Inc, I checked their profile but the available information is very less. What I’ve seen is that their growth rates are/were high in the last 2-3 years and I think before that they were very small (infact tiny).

(Consumable Ranked Number 32 Fastest-Growing Company in North America on Deloitte’s 2020 Technology Fast 500. Attributes 7,174% Revenue Growth to its Unique Ability to Blend Short-Form, Bite-Sized Entertainment into Digital Advertising

Consumable, the leading content discovery platform, today announced it ranked 32 on Deloitte’s Technology Fast 500™, a ranking of the 500 fastest-growing technology, media, telecommunications, life sciences and energy tech companies in North America now in its 26th year. Consumable grew 7,174% during this period.)Looking at this high level of growth from a value investor’s perspective, I’m not sure whether it would be good to pay more than $100M for a company that grew it’s revenue 71 times in a very short time. In investing I won’t buy a company’s stock if its revenue increases many times in just a year or two. Most important thing here is that it depends on whether the growth is sustainable and whether the business is scalable. If the above can be done then I’ll be wrong in my assessment and I’d be a fool to miss out on that opportunity. Like I’ve mentioned above, there’s not much available information about the company to do any type of analysis. Their website is very informative in what they do and being a private company it’s obvious that there’ll not be much information about them. I can’t judge whether JV is better or outright acquisition would’ve been better but I’ll leave it to experts who work on ground and who know the technological trends.

And I’m guessing, if they acquired both Mediamint and audio assets of Consumable Inc then there wouldn’t have been any funds left and would’ve put the company in a difficult position. They’d have to spend close to $150M cash on both these. All the funds would’ve to be spent on these and once you acquire these you need also have to worry not only about your present working capital but also on these companies’ working capital. To manage that you’d again have to take on debt or issue more shares.

I’m the biggest supporter of buybacks (but not dividends) but when you have opportunities like audio ad (podcasts and streaming), presidential elections, and threats like ChatGPT, credit crunch, recession etc it’ll be better to concentrate on business and instead of dividend let them buy back shares. Once we are past that and when the company is in a better position it can pay more dividends. Also, dividends (and buybacks) are temporary solutions. I think a better solution to save cash would be ESOP, instead of paying cash to employees they can buy stocks from the market and give them that instead. If the stock is this volatile I’m not sure whether employees would agree to that. Most of the companies in the US give shares, though they don’t buy from the market but instead issue more shares.

Look at how the market treats and trusts Affle which doesn’t pay any dividend.

May 22, 2023 at 2:53 am #26062LoganRegistered BoarderI forgot to mention a very important point. Last year (2022) BCG paid 30 paisa (0.3 rupee) dividend and the total amount was little over Rs.60 crores. In 2020 it was 5 Paisa (or 0.05 rupee) and the total shares were 50 crores so the total amount paid was just Rs.2.5 crores. In 2021, it was also 5 paisa but maybe for double the number of shares so total maybe around Rs.5 crores.

Increasing total dividend paid by 24 times in 2 years

(2.5 crores to 60 crores) and 12 times in a year (5 crores to 60 crores) didn’t change the sentiment about the stock and the whole sentiment was based on 3 very important factors which I’ve mentioned in my previous post, which are FA, SHP and corporate governance issues. Fixing issues and being more honest, open and having transparency would’ve had better results than paying dividends (which I always say).Also, BCG’s total dividend paid is more than what many companies make in profits in a year which still didn’t convince the market.

We have to analyse what the problems are and those problems will be different for different companies. Paying more dividends is a generic solution which doesn’t suit all the companies. It may set a narrative that dividend paying companies are stable but it hardly solves important problems.

And the company’s stock had a better performance when it paid off all the debt (and when it paid total dividend amount of Rs.5 crores) than when it paid 60 crores as total dividend amount. Though circumstances were different in both the cases, my point is that the market will cheer when there’s less uncertainty about companies and when they close pending issues.

Last year when the dividend was announced the stock was at 60 or 70 but look where it is now.

If there are 10 important things for the company to get a good valuation, dividend will only be one aspect and there’ll always be other important things and most of them will be about transparency, governance and growth and stability in the business.

May 22, 2023 at 10:33 am #26063NIRAJ1Registered BoarderAdded few shares today at bottom price. Holding good quantaty.

8+May 22, 2023 at 5:51 pm #26064jmathewRegistered BoarderFCF

Q1 205cr

Q2 216cr

Q3 92cr

Q4 pending receivable from Q3 (100 cr) + Q4 (200cr) = 300 cr

Total FCF q1+Q2+q3+q4=813cr

15% will be around 120cr.

So they may declare a dividend of a minimum of 50 Paisa.

Let us wait and see.12+ -

AuthorPosts

- You must be logged in to reply to this topic.