Tagged: Call Girl Rishikesh

- This topic has 5,566 replies, 167 voices, and was last updated 7 hours, 37 minutes ago by ImensoSoftware.

-

AuthorPosts

-

February 8, 2022 at 11:59 am #13157hw_twRegistered BoarderFebruary 9, 2022 at 1:11 am #13159hw_twRegistered Boarder

The Digital Marketing divisions of Hearst group is somewhat matching with the PR details shared … Hearst is similar to Times group with interests in TV, Radio, Newspaper, Magazine etc;

Some portions of PR narrative shared … Like the details about audio ad industry can be seen in this Hearst Bay Area site

https://marketing.sfgate.com/resources/rise-of-digital-audio-advertising?hsLang=en

And the Google, Microsoft Partnerships can be seen at their HearstDMS site

Probably BCG is acquiring some of these divisions … Its just a guess as of now … there could be other similar companies too ?

February 10, 2022 at 10:31 am #13163whySharesRegistered BoarderMy view of the present situation

The crash in BCG share price is because the preferential shareholders have a lockin period of one year on the shares allotted to them through preference issue, but the bonus they get on those shares have no lockin period. The SEBI rules on lockin period for preferential shares is very clear, but there is no rule regarding bonus shares on locked in preferential shares.

Many feel that the preferential guys will try to recoup their capital by dumping their bonus shares in the market once bonus is issued and there will be a big fall in prices because there will be too much dilution when all these shares come together in the market.

As investors we just have to wait it out. One or two months after bonus issue the value of your holdings will keep on rising.

This is just my view of the present situation.

Usual disclaimer – share markets are subject to risk ———3+February 10, 2022 at 1:11 pm #13166whySharesRegistered BoarderMy above and the following comment is pure speculation by me. Please comment on whether it could be correct or not.

Many investors are also angry about the preference shareholders bonus shares not being locked in. They feel the management issued the bonus shares to favour the preference share holders. I don’t blame the management, because the money brought in by the preference share holders has helped BCG to grow, by buying some high profile companies, which will accelerate the growth of BCG in future. One of the preference share holder, Shanker Sharma, was responsible for the rapid rise of BCG from 37 to touch 200. Now we need to have patience and not worry about BCG going down to 130 levels, may be!

4+February 10, 2022 at 1:15 pm #13165kiranRegistered BoarderThe preferential allottee will see the micro data , with respect to its peers also while selling the bonus shares . Any investor will see the PE ratio, EPS of BCG wrt to Affle , tradedesk which will be quite cheap then. By Q1, FY 2023 , free cash flow of BCG will be Rs 500 cr +. The fundamental of company will arrest the fall in price as underlaying has value in it.

With disclamer : stock market is subject to risk.February 10, 2022 at 7:10 pm #13168NIRAJ1Registered BoarderEmail sent to BCG Management for action.

10-2-2022

Dear sir/madam,

Please send my message to Management. I am an investor who invested IN BCG for the last 7 yrs.

1) To give Bonus to attract new realtor investors is not successful 2nd time within 1 yr. Please cancel this strategy to recover the price of the company.

2) E&Y is auditing 40-50% of income till today and other by local auditors. Now BCG is large cap company. To increase trustability of the Audited figure of BCG, Please appoint E&Y for the whole company which is the demand of time and also by retail investors. Few people increase doubt due to this point and create negativity and create havoc as you have seen this time in price.

3) For acquisition you need money. Either you take a LOC of 150$ million -loan or consolidate subsidies at USA level and sell some stake. You require an authentic audited figure to work it out.

Please consider these points sincerely for BCG’s progress.12+February 11, 2022 at 2:56 am #13171LoganRegistered Boarder@whyshares, I think preferential holders will have lock-in period for bonus shares as well. Some PW holders were allotted shares before bonus shares were issued and they still have lock-in periods.

One example – when BCG released SHP on 1st July-21, PANKTI COMMOSALES LLP had 1cr shares (pre-bonus) locked-in and now they have 1.25crs shares locked-in.

February 11, 2022 at 11:09 am #13173NIRAJ1Registered BoarderDear Logan,

we agree that BCG has doubled its business from last 2 quarters. Now company needs money for payment. Earlier SKR said that we dont take Business due to liqudity crunch. Due to preferential allotment of shares, company got money and BCG took extra business and quarter result are showing great result. so lot money used to bring new business. Your calcualtion is right for incoming money but it is used for expanding business.

New allotmetn of FPI more than 10crs shares brings around 330cr which is used for mediamint acquastion.

Now Audio company acqusion BCG needs money. She willl have 500crs by 1st quarter of 23 and i agree it but what about additional payment? I think there will be short of 300crs. This is my thought procees.Coreect me if you find any mistake of my calculation.2+February 11, 2022 at 3:07 pm #13176whySharesRegistered BoarderFII share holding now 11.5% campared to almost NIL one year ago

Very soon FII will corner more shares and there will remain very few floating shares – a recipe for astronomical rise in share price6+February 11, 2022 at 7:12 pm #13177hw_twRegistered BoarderA wonderful discussion with Aditya Vuchi on his MediaMint’s journey and the lessons learnt in building a 1500 people / India’s the largest Digital Marketing agency (did he said that ..?

Lot of insights to learn from, whether you are a startup person or a investor especially a BCG investor … I really liked the clarity of thought he has

Request everyone to please watch it and also share it

Teaser … He talks about US vs India business, Services vs Product business, Market size, Profitability, People, Strategy etc;

February 15, 2022 at 11:03 am #13179hw_twRegistered BoarderSet of events from BCG in next two months

In next one month

– Closure of MediaMint acquisition post cash payment– Bonus record date announcement

– Mr. Shankar Sharma’s balance 75% payment for warrants before the bonus record date

– Investors presentation from SKR as stated in the concall

– Earnings, FCF, ROE guidance figures from SKR for the next FY

In next two months

– Announcement of Audio AdTech company acquisition post closure of legal, financial due diligenceWe might hear some more news items like BCG inclusion in different other BSE, NSE indexes, FIIs / MFs additions, MF research reports, Leadership hiring, Product updates etc;

February 15, 2022 at 1:49 pm #13181odyseeRegistered BoarderA pathetic display of unprofessional interviewing by CNBC-TV18.

Discourteous and with no understanding of the nature of the industry that BCG operates in.

The apparent objective was to undermine every statement and explanation being provided by Mr Reddy without any attempt to even understand the content of the answers.

To say that I am disgusted with the behaviour and approach of the ill informed interviewers will be an understatement.February 15, 2022 at 5:05 pm #13183JackSparrow13Registered BoarderSaddened to see this interview. Normally, Mangalam Maloo raises for the right, but this time he seems more interested in getting cheap publicity. I do understand paying no dividend can raise a red flag. But paying low dividend cannot be a issue. Why should a promoter with low promoter holding waste money in dividend (feeding minority shareholders and government). Buyback can be best, but brightcom will not be able to afford a buyback (capital needs to allocated to growth, as well as equity size is so huge, buyback proportion will seem a joke). Not everyone can be Messiah of Investors like suppose Dr.Vijay Mallik. Trying to make paint a company as criminal, because street perceives it to be, is being fundamentally dishonest to one’s job.

Damn sure Brighcom’s rise will burn a few asses, and will be great fun, becoming rich and seeing naysayers needing tons of Burnol. May them be hit with Thousands of Thundering Typhoons, and suffer from Billions of blue blistering barnacles!

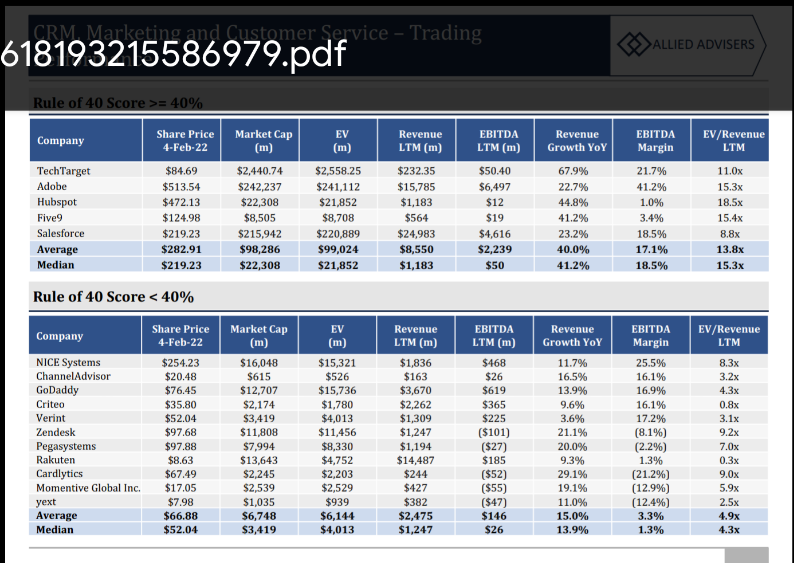

…Sorry, got a bit carried away in emotions…February 16, 2022 at 12:40 pm #13187February 16, 2022 at 1:02 pm #13188hw_twRegistered BoarderBCG’s last 12 month’s growth + EBITDA margins is way above > 40%.

As per the Rule of 40 for SaaS companies, BCG’s valuation should be in the range of 13.8x to 15.8x EV

BCG has clocked 4479 Cr sales in last twelve months (LTM) … Its valuation should be in the range of 61,810Cr to 70,768Cr

February 16, 2022 at 5:16 pm #13191myainvestRegistered BoarderShares are in strong grip of some operators who desperately want to pull down the share price. One can easily observe, that whenever share price rises, suddenly the operator will put big sell order for eg, 40K order at rs.145 – it comes to around 58 Lakhs approximately for 40K volume. And it will take some time to be observed by retail – not all retail can afford to buy it. Before it gets observed, they deliberately put another sell order at 143 for 20K for example. They repeat the same things till it get locked in LC. Once the share is in LC, more retail will panic and volume will increase. Operators are doing the same since 180+ and brought it now to 140. Not sure when this is going to stop. All big players percentage are still the same as per latest shp. Sometimes, I hate giving too much shares in the hands of retails – they don’t deserve to be rich.

16+February 16, 2022 at 11:33 pm #13193ramganesh1982Registered BoarderHi All,

This is one of the most unprofessional interviews I have ever seen . It was like a Hollywood / Bollywood / tollywood movie where the interviewers assumed themselves to b some sort of CBI’s who wanted to expose one of the biggest scams, just by asking their interview questions (should backfire them soon) . They want to become world famous overnight and want to create that wow effect. Fools don’t understand the nature of business ..nor do they compare with peers on receivables .. I wish skr asked them back some stronger questions .. like ” do you really know how much dividend Google pays ?? ” ” Have u ever seen the receivables of other ad-tech companies ??? ” .. he was too polite to them .. should have fired back some strong questions .. it’s a matter of time before bcg bounces back even stronger

Regards

RamFebruary 17, 2022 at 10:25 am #13194whySharesRegistered BoarderJust a contra question

Could it be possible that the CNBC interview was deliberatly negative, with the agreement of all, to drive share price down? The aim: to create a buying oppertunity to vested interests12+February 17, 2022 at 10:50 am #13195chrisRegistered Boarder@whyshares that would definitely affect the overall sentiment that’s been built around the share (my opinion), if you are implying that the management has willingly agreed to this.

My opinion NO because none of these questions were new, they have been answered again and again in a lot of con calls so many times that it is exhausting to even listen to the same question. A similar opinion was aired by an anchor in a Telugu news channel who invited SKR after the acquisition of mediamint and apologised publicly. The ignorance and arrogance of holding a Mike on a platform CNBC tv 18, isn’t new.

February 17, 2022 at 12:23 pm #13197hw_twRegistered BoarderWhen you have not done a detailed study of the company, its business model and the history … you will end up with questions with lot of ambiguity … and also you will not be in a position to understand the answers provided by the other party

Regarding question related to BCG’S biggest clients …

BCG directly and indirectly works with different parties … Like Publishers, Media Agencies, Digital Marketers, Brands etc;

In this context, it becomes tricky to understand what the interviewer is exactly looking for … I mean, is the interviewer asking large clients in terms of a big names across these different types of clients or only from a particular type and is the question is about large client in terms of big brand name in general or a big brand name which the interviewer is aware of (like Google, FB, Unilever etc;) or large client in terms of revenues

SKR has answered this question with the names of Media Agencies they are working with like MediaCom, Havas, Mindshare … But the interviewer could recall only names like Google, Yahoo, Unilever which they know

Also some of the questions indicates that they were not prepared well … Or they have a pre-determined judgement … and were also rude by not allowing SKR to answer questions … Will discuss this further

-

AuthorPosts

- You must be logged in to reply to this topic.