Tagged: Mumbai escorts service

- This topic has 5,566 replies, 167 voices, and was last updated 2 weeks, 1 day ago by Logan.

-

AuthorPosts

-

January 20, 2022 at 11:33 am #13087nitin_asceRegistered BoarderJanuary 20, 2022 at 11:48 am #13088YogiRegistered BoarderJanuary 23, 2022 at 9:36 pm #13092kiranjRegistered Boarder

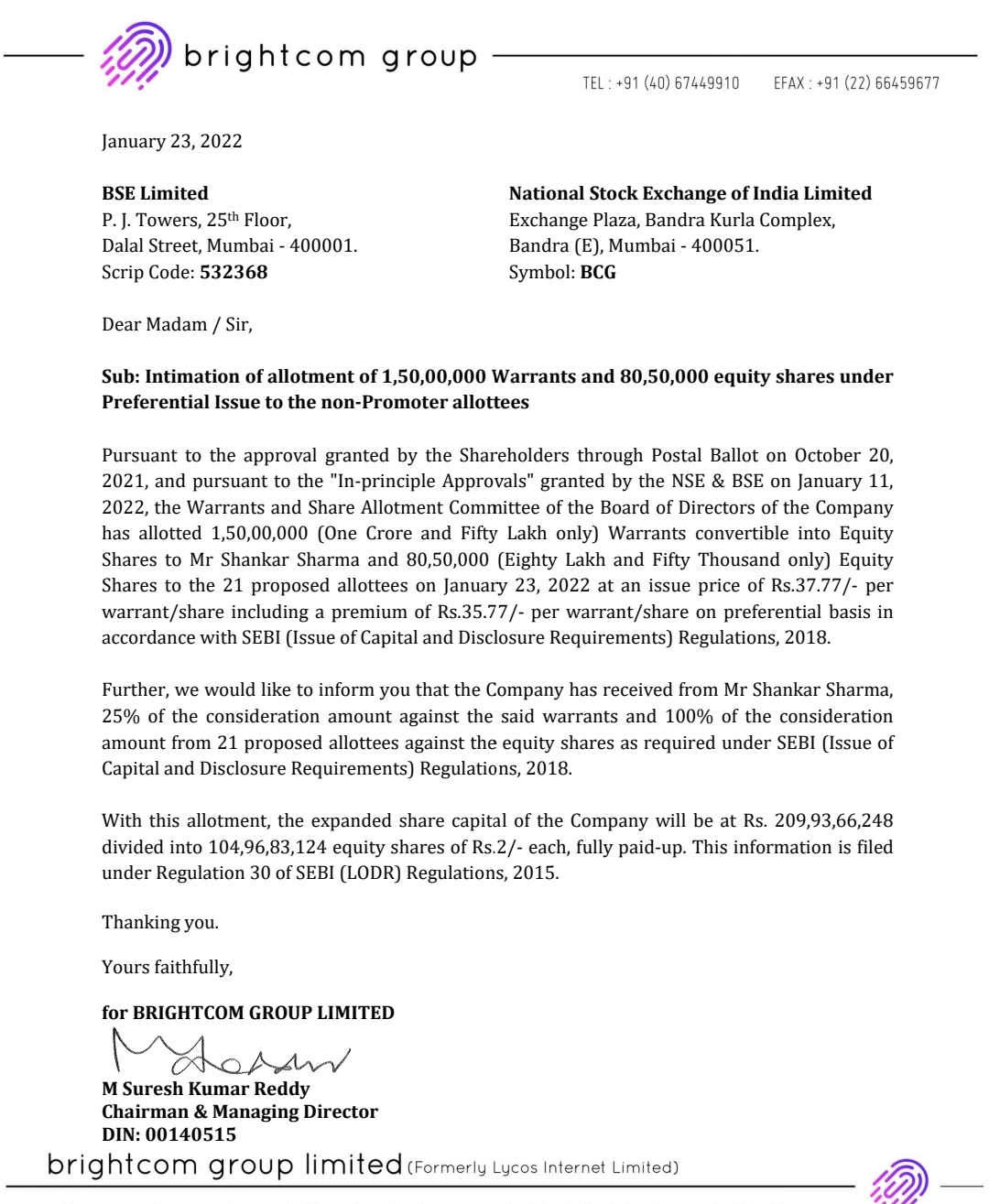

Hi All Mr Shankar Sharma alloted 1.5 crore preferential warrants at 37.77 Rs . He has already paid 25% for the same. FPI’s allotment will also happen soon I think. Cheers

Attachments:

January 24, 2022 at 5:17 pm #13094NIRAJ1Registered BoarderShankar Sharma have interview on CNBC today and have logic for investment in

BCG at 37Rs.. Here it..

httpss://youtu.be/qge0HPblUwI9+January 24, 2022 at 7:05 pm #13095kiranjRegistered BoarderJanuary 24, 2022 at 10:43 pm #13096VALUEBUYER001Registered BoarderAny one please clarify whether bonus that would be issued on 33 crores pw converted equity shares with lock-in upto August 2022 and 14 + 1.50 crores shares issued to fpi and shankar sharma with lock in of 1 year, will also have lock-in or free to trade.

3+January 25, 2022 at 6:03 pm #13098vgsatworkRegistered BoarderRegarding Bonus issue – Earlier today, company notified that with today’s preferential share allotment, # of shares is currently at 116 crores. Given that last year in the run up to EGM, maximum share capital of the company has been revised and approved by share holders as 300 Crores, which would be 150 crores of shares. Given that pending Preferential share allottees and Shankar Sharma pays up on time to be eligible for Bonus share, the equity base would be 120 crore shares which would leave room for essentially only 1:4 for kind of bonus ratio, unless company decides to revise the overall share capital upwards. Such a move would require a General meeting (EGM to be precise since AGM happened hardly a month back) and change in company’s Article of Association.

Given that Company had made it clear that they may not dilute the equity any further and such dilutions have direct impact on the RoE which company said is a key metric that they would be tracking hence forth, it is very likely that the company may settle for a bonus ratio which is less than 1:4 to avoid increasing the overall share capital in excess of 300 crore, which was approved in EGM hardly 7 months back.Despite all these, if the company announces a bonus ratio of 1:2 or 1:1, which is a direct indication about the growth momentum that they are seeing on the ground and the7ir ability to keep RoE in excess of 17-18% and that would be a very clear indicator for all the shareholders w.r.t the growth prospects.

Hoping to see 1:1 bonus announcement…

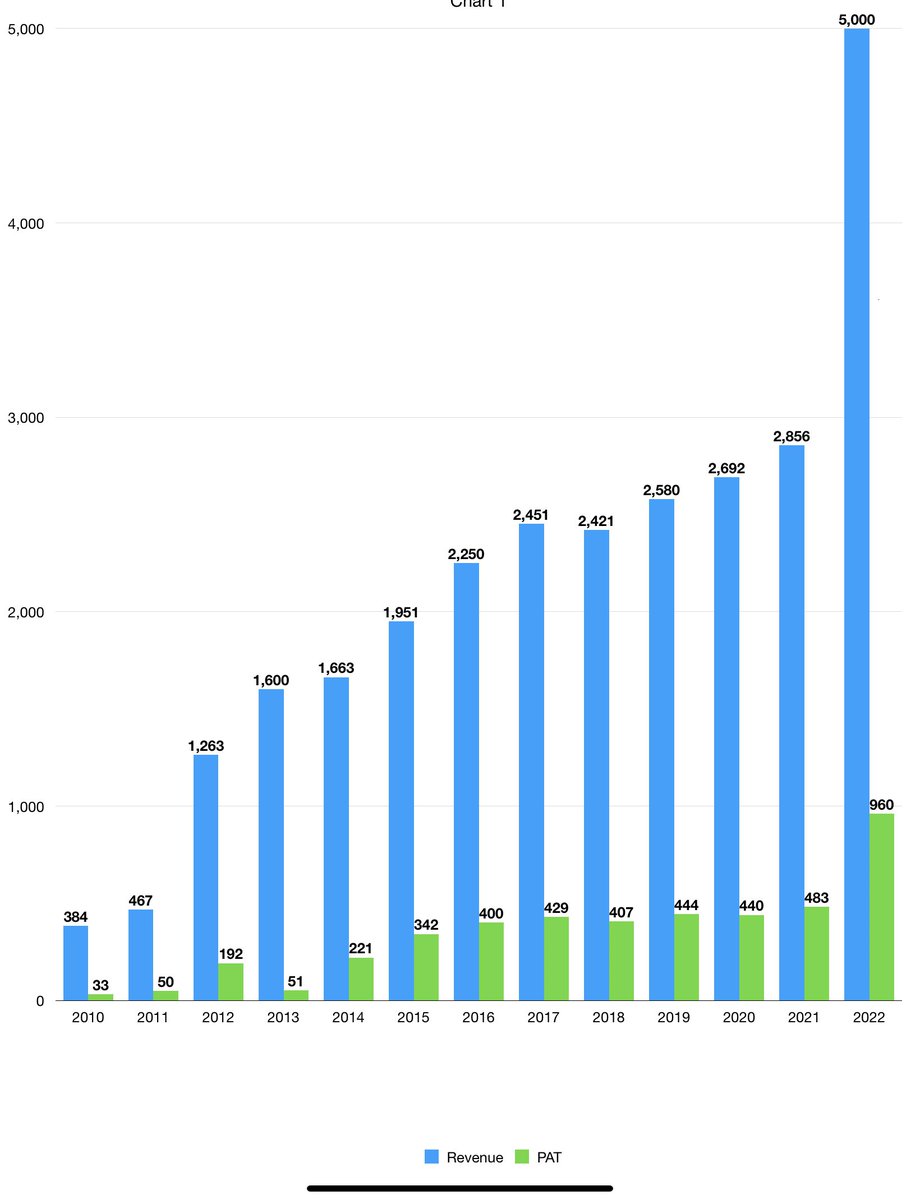

January 25, 2022 at 11:59 pm #13099AbhishekRegistered BoarderJanuary 25, 2022 at 11:59 pm #13100vgsatworkRegistered BoarderBCG has shown fantastic results and have given 2:3 bonus, representing 66% rise in equity base. The signal is very clear that the company is seeing phenomenal growth ahead. Domestic and foreign institutions cannot stay away from this post these numbers. Expecting rapid PE rerating given over 165% YoY growth in bottomline and 130% topline growth on a fairly large base. Expecting PE rating to reach 40-45 range based on Trailing twelve month EPS of 8 rupees implying a share price of around 350/- pre- bonus and post bonus price of around 210 or so.

January 26, 2022 at 9:31 am #13101hw_twRegistered BoarderCongratulations SKR gaaru and the entire BCG team for delivering Blockbuster results

ROE of 21.74%, EBITDA margin of 25% with 130% growth in Revenue and 169% growth in PAT beats any other tech company performance you want to compare it with … on top of it a 2:3 bonus with a re-affirmation that BCG is going to generate 500 Cr FCF in next two quarters … What more you want

SKR has consistently outperformed guidance numbers for the second consecutive time … especially given that the guidance numbers itself are very high and with all the uncertainties around pandemic, lock downs, consumer spending etc; he has still delivered

As I said before, once you have boarded the ship Trust the captain of the ship … SKR is like “Pushpa” when it comes to performance and he is like “Bahubali” when it comes to rewarding the investors

Hoping all the intelligent investors out there will take a note of all positive aspects of BCG and get into the ship as soon as possible and be part of the historic story unfolding … and also please do support the management with your constructive feedback

January 26, 2022 at 10:07 am #13102odyseeRegistered BoarderWell summarised @hw_tw.

You have articulated what must be on the mind of all on this forum and the larger retail investor community beyond.

This is truly an incredible performance by Team Brightcom, so ably led by Mr Reddy.

To give a performance guidance for 3 remaining quarters so many months ago was a frightfully brave and ambitious move by Mr Reddy, and apart from the incredulous joy experienced by us all, I’m sure that the intensity and numbers of ‘fingers crossed’ has resulted in quite a few sore digits at this point.

The sheer audacity and determination and belief and commitment and excellence demonstrated by the brilliant Mr Reddy and his colleagues in the Brightcom family deserves a standing ovation from all stakeholders.

Take a bow , Mr Reddy.

And we are confident that the best is yet to come !!

I would be amiss if I were to not express more than a word of appreciation to all fellow forum members and Admin and Logan for keeping this passionate and informed group so very relevant in this incredible and rewarding journey.January 26, 2022 at 6:57 pm #13103hw_twRegistered BoarderRegarding BCG vs Affle’s cost per converted user, SKR has already answered for this question in Q2’s concall … BCG is into both Cost per Impression / CPI and Cost per Action / CPA models … Note that CPCU model is a bit more than CPA model where in the user is tracked till the end … also cost for each of these models keeps increasing from CPI to CPA to CPCU models … for simplicity stake let’s assume CPA and CPCU are in the same category

Both these models are good for different campaign needs … it depends on the type of campaign which the company or brand is looking into

Awareness campaigns target is just to let people aware of certain product or event and it doesn’t expect any immediate action from the viewer … basically they just send a message across targeted group of people … CPI ads are good in this case

For example, campaigns done during election time asking people to vote for a particular party, leader or asking to participate in elections or a vaccination campaign fall under this category … you just need to run an ad, over here … there is no need for the viewer to take any action … even ads like launch of a new mobile or an IPL match would prefer normal CPI ads

On the other hand, Action campaigns target is to get the user do some action like subscribing for a service or purchasing etc; … Note that these are subset of normal awareness campaigns … the challenge in this model is that you will have to run lot of ads for the actual action to happen … because of which the prices are high … the margins become unpredictable as you never know whether the viewer is going to take an action after 10 or 20 or 100 ads or he may not take any action at all as he has already purchased the product

My personal experience which happened every time I wanted to purchase a product and I am sure most of you would have faced this … When I wanted to buy a product, typically I would check for the product price it’s features and also check the competitor’s products in the same or different price ranges … the movement I do this, I will be chased with different product ads across different other sites I visit through out the day … Inspite of all the ads, everytime time I end up purchasing a product directly from the ecommerce site or the shop which I liked and NOT by clicking on any of the ads … The biggest thing over here is that you will be chased with these product ads even after a purchase and this continues even after a month or nore … 🙂

During this period, I would have visited multiple websites … Probably in a month I would have seen an ad for some 1000 odd times … In a cost per impression model this cost would be in single digit rupees whereas in a cost per action / CPA or CPCU model this would go to double digits say 50 to 100 rupees as mostly lot of people like me would have purchased the product directly without clicking on the ad shown by the Adtech company … Note that in CPA / CPCU model, this cost has to be borne by the Adtech company like BCG or Affle … typically they end up chasing 5, 10 or 20 people before they find a buyer making a purchase through their ad and these acquisition costs shoot up for them

If you look at it from the Adtech companies perspective, a normal cost per impression model is more advantage for the Adtech company … having said this Affle seems to have done lot of work on understanding customer demographics and running a smart ad campaign cutting the costs involved and they seem to be doing good in this space … But, when we look at the overall market size this space is small and is a risky one compared to CPI model which BCG is largely into

In a nutshell the point to note is that there is a need for different types of campaigns … In cases where there is a scope for both types of campaigns the Brand manager along with campaign manager might be deciding which one to run or would do a split between both … from the Adtech companies perspective they should be ready with services for both the options

Hope this clarifies on the difference between these two models and the cost benefits from the Adtech’s POV

January 27, 2022 at 9:52 am #13106RajaRegistered BoarderFebruary 3, 2022 at 2:25 am #13131AbhishekRegistered BoarderLogan sir .. you articulated very well with Excellent example as always. rightly said that naysayers are taking advantage to misguide people and impatient investors. I laugh on their analysis referring past issues which are closed already. Good part is now through this forum and company’s exceptional performance and after shankar sharma, this stock is getting popular day by day. Market has to recognize good fundamentals stocks, and so BCG will definitely achieve its right valuation in a year time.

February 3, 2022 at 7:30 am #13132SaachRegistered BoarderFebruary 6, 2022 at 9:36 pm #13141RajaRegistered BoarderFebruary 6, 2022 at 10:05 pm #13142vgsatworkRegistered BoarderGreat news. Does anyone know the difference between share purchase transaction and asset purchase transaction?

Does it mean BCG is buying a portion of the business (assets/liabilities/employees,etc) for cash consideration from a US Company that is dealing with digital audio?

4+February 6, 2022 at 10:33 pm #13143AbhishekRegistered BoarderLet me remind our all investor friends, SKR sir told very clearly 2 quarters back that by Mar 2023, he along with his team will put everything as per their plan (shared with us) in place and at that time true EPS, Cashflow and shareholding pattern will reflect. He has put a great strategy in place and now we can see all action items getting closed one by one as per his plan. Also with this growth journey, he is taking care of shareholders by rewarding with bonus shares and dividends too. Hats off to SKR sir and his team.

Happy Investing!February 7, 2022 at 9:49 pm #13155hw_twRegistered BoarderOne more good news in the form of US based Audio AdTech acquisition … my views on the info shared related to this acquisition

– Acquisition cost of 7X EBITDA is inline with BCG’s previous acquisitions

– 33.3% EBITDA margin … Inline with higher margins as mentioned by SKR before … It’s higher than BCG’s existing margins which is around 28 to 32% … also higher than Affle’s margin range of 20 to 25%

– It’s revenue CAGR growth is not given … the comments on active users of 200 million in US and reaching to 1.5 billion across the world indicate a good growth of this industry … hope we will get these details when the deal is signed

– The target company already has tie ups with Google, FB and Microsoft … Indicates it’s an established player … also Mr. Satish Cheeti highlighted that these are successful assets

– It is mentioned that “The synergies between the current Brightcom

business and new assets will add to the above numbers.” … Some possible synergies could be– Given that the target company is currently operating only in US and has a lot of scope to expand all other countries including India

– BCG can move some of its existing audio ad contracts to this new platform

– Also it can help their existing publishers with additional monetization option in the form of audio adsThe overall deal will close by next 4 to 5 months (legal and shareholders, board approvals steps) and the revenue will start adding from Q2FY23 onwards … Basis previous years numbers this will add 250Cr minimum to the topline for the next FY … Considering a conservative growth of 30% to 40% range this will be between 325Cr to 350Cr topline addition from this division … any synergies with BCG’s existing clients along with its agencies and MediaMint will be on top of it and this in my view would positively surprise us ..:-)

BCG is the most undervalued company compared to any listed Digital / Platform companies or for that matter even with the Digital transformation service companies … It is already doing well in comparison to others in terms of growth rates, EBITDA margins, FCF etc; … these two acquisitions has further widened this valuation gap and there is a lot of scope to catch up

February 8, 2022 at 11:57 am #13156hw_twRegistered BoarderThe target Audio AdTech company is a Google’s Premium Partner … It is the highest level of partnership and is reserved for top 3% of the partners

https://www.google.com/partners/become-a-partner/

Same is the case with Microsoft … Its “Elite Partnership” program is the highest level

Both these partnerships indicate the strength of the team and the quality of customers they are working with

@vgsatwork – This also confirms that the acquisition is including their employees who are trained and certified in these technologies … probably they might leave out a small percentage of employees provided this work is taken over by their Israeli or Indian team including MediaMint -

AuthorPosts

- You must be logged in to reply to this topic.