Tagged: Call Girl Rishikesh

- This topic has 5,566 replies, 167 voices, and was last updated 2 days ago by ImensoSoftware.

-

AuthorPosts

-

May 12, 2022 at 8:59 am #13986May 12, 2022 at 9:08 am #13987JackSparrow13Registered Boarder

I did not understand this clarification at all. Really dont trust the timelines, given by management. Was this a issue of preferance shares not getting subscribed/paid, even after bonus announcement?

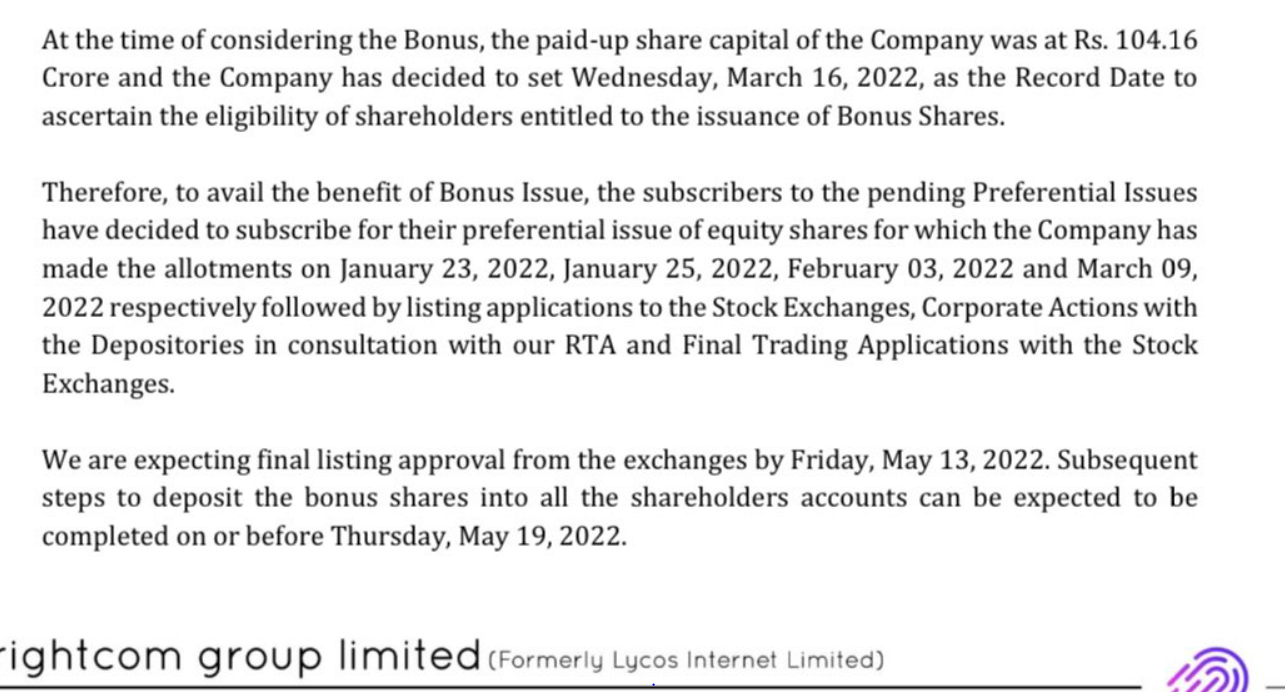

Attachments:

1+May 12, 2022 at 9:44 am #13989myainvestRegistered BoarderMay 12, 2022 at 9:46 am #13990chrisRegistered BoarderAs per the notification released, full payment of the subscribed preferrantial issue was done according to the dates mentioned, before the record date. The delay/issue has been listing of these shares on the exchanges before final allotment of bonus shares (my understanding of the press release)

Suresh reddy’s tweet “ do expect more updates from us in subsequent days “, sounds interesting.May 12, 2022 at 9:47 am #13991LoganRegistered BoarderI think we should appreciate Zee Business channel for getting the management people to act quickly. Though this bonus issuance incident should not have gone this far in the first place. Hope this will make them to avoid these kind of things in the future.

May 12, 2022 at 9:49 am #13992sac6310Registered BoarderSKR in his below tweet

We sent the following notification to the stock exchanges regarding the bonus shares issuance and credit. Do expect more updates from us in subsequent days. #Brightcom #BrightcomGroup pic.twitter.com/Sl4SfSdsf4

— Suresh Reddy (@suresh_66) May 12, 2022

mentioned that ” Do expect more updates from us in subsequent days.”

Does he is indicating for updates on bonus only or for other good development/surprises too.??May 13, 2022 at 11:40 am #13994chrisRegistered BoarderThere is a recording of SKR in a telegram group (v2w), where he is trying to clarify to an investor regarding bonus and SHP.

In summary, what he’s saying is that there’s nothing wrong we’re having issue after the CS (Manohar) has resigned but he is still helping me as a consultant.

Bonus will be credited by 19’th of this month and subsequently all doubts regarding the SHP will be clarified and explained.Couldn’t share the clip as the telegram group does not allow to either copy or forward.

Here’s the link if anybody is interested …

May 14, 2022 at 11:52 am #13995BrightspotRegistered BoarderChris would you mind sharing what did SKR told about SHP in the call, we are unable to join telegram group thank you

3+May 14, 2022 at 1:03 pm #13996chrisRegistered BoarderSorry the telegram group does not allow forwarding or copying any of the messages posted on it.

So the gist is SKR calls the investor (who I think called previously and was maybe rude to the person answering the phone at the bcg office) and tells him that the bcg office is not equipped to take in a load of 3 lakh investor calls and that’s the reason they were unable to respond. He assured him that they would set up a mechanism to deal with this in a weeks time.

He requests the investor to stop spreading unnecessary negativity and panic, he assures him that everything is fine and there is no problem at all. There is a chat about the zeebusiness coverage of bcg.

Finally, the investor asks about the SHP and promoter holding to which SKR says that he will explain about it in due course and nothing is wrong, quarterly results and concall he be held as per schedule.

May 17, 2022 at 8:35 pm #13997chrisRegistered BoarderSo, finally bonus has been credited will list in a couple of days for sure now, market looks like it might bottom out for now, but then again brightcom stock movement was always independent of market direction up until now.

So upcoming brightcom notifications in order of most significance would be

1. Audit report.

2. Mystery of disappearing promoter holding.

3. Update on Audio advertising acquisition.

4. Quarterly results.

5. Guidance report for upcoming year.So what do you guys think, please do add to the list which I guess can be used for clarification during concall, tentatively in the first week of June post quaterly result release.

13+May 18, 2022 at 11:07 am #13998chrisRegistered BoarderConnecting dots 29

SWOT Analysis of #Brightcomgroup #BCG

Below analysis is my personal view and so do your own research for your investment

Open discussion is healthy@suresh_66 @1shankarsharma @peshwaacharya @tsurendar @BrightcomGlobal @BrightcomGroup @BrightcomInvest https://t.co/JYkxVYN8Mx pic.twitter.com/WvvcCT41Np

— Happy_Hindustani (@Happy_Hindustan) May 17, 2022

Detailed SWOT analysis on brightcom. More importantly an unbiased view.

May 20, 2022 at 12:53 pm #14004whySharesRegistered BoarderIn an article published on ET Prime headlined “Stellar returns or just a mirage? How Brightcom’s fundamentals don’t support its valuation”

Quoting some stements which need to be addressed

1.

“Suresh Reddy, its founder and promoter — a technocrat based out of Hyderabad, sold 90% stake in the company, which eventually reduced the total promoter stake by 4%, but warrants were also exercised. Hence, the total number of shares for the company increased by 16 crore.”2.

“While the ad-tech business is on a growth path, the company’s fundamentals are shaky. Brightcom has huge receivables on its balance sheet that are worrisome. Around 56% of the total current assets are trade receivables and 34% is accounted for loans and advances. The present sales-to-working capital ratio works out to less than 2x, which shows that there is a lot of pressure on the running cost of the business. ……

……..

There is nothing wrong with this. It is a commonly followed practice because the company eventually receives its payment. But there is a maximum waiting period beyond which it makes little sense to keep writing in the accounting books as ‘receivables’. Account receivable days is the metric used to calculate the number of days before which the company receives its payments. This number depends on industry to industry.Pharma has an average 68 receivable days, for manufacturers like capital goods it is 77 days. IT, which is more of software services, has an average 62 receivable days. For the Nifty 500 companies, removing one outlier Vakrangee, the average trade receivable days number stands at 55. But Brightcom has 142 trade receivable days — this is two and a half times the total average.

Not only that, Brightcom’s trade receivables, which was at around INR750 crore from FY12-FY17, increased slowly thereon until it shot up in FY20 and FY21.

“High trade receivable days don’t work very well in the long term in terms of its impact on revenue,” says Abhay Aggarwal, founder and fund manager, Piper Serica, a Sebi-registered portfolio-management service (PMS).

Loans and advances

This metric falls under non-current assets in the balance sheet. As the name suggests, it is the loans or advances given to receive them in the future with interest. This number stands at INR720 crore for Brightcom for FY21, which is almost 20% of its total assets.”3.

“Free cash flow or FCF is the cash available with the company after all the expenses for working-capital requirements and capital expenditures are met.Both trade receivables and loans and advances together constitute 62% of the total revenue. This is not just for FY21 but has been the case since FY18. And since the receivable days are long and loans and advances are huge, they have directly impacted the FCF.

FCF can be negative for one or two years, but it cannot be the same for an extended timeframe. In Brightcom’s case, FCF has been negative for a decade. This means the company has not generated cash in a very long time.

Summing up, the revenue numbers look inflated. Perhaps that is why mutual funds have not touched the stock, while long-term individual investors sold their stake at the very sign of ‘exit’.

4.”Should one invest in this stock?

Based on fundamentals, the company has a long way to go to command its present valuations. The fact that the business has not shown any growth in an environment where tech-related companies are growing at a rate of 15%-20% annually over the last five years, Brightcom shows little promise. The promoter has sold out much of its holding. This does not look good for new investors who want to buy the stock.With a Sebi investigation calling for a forensic audit and more questions about the growth of the business, investors need to be careful before they take any investment decisions.”

May 20, 2022 at 1:40 pm #14005odyseeRegistered BoarderIt’s getting tiresome playing defence incessantly.

In absolute terms, an analysis like the one discussed above can be believable by investors not familiar with BCG or the unique nature of the digital advertising business , and its bias is visible only to the ones who have closely followed all developments in recent years.

A strong point by point rebuttal is required, else the perception being created is resulting in continuing destruction of shareholder value and reputation.

Millions would have read the ET article, but very few the positive comments on this forum.

Proactive communication is the need of the hour Mr Reddy, irrespective of the current challenges being faced by you and the company.May 20, 2022 at 3:06 pm #14006safRegistered BoarderPublished on May 18 2022

Below is the copy of text from the article. you can read the article in the link also directly.https://simplywall.st/stocks/in/media/nse-bcg/brightcom-group-shares/news/is-brightcom-group-limiteds-nsebcg-shareholder-ownership-ske“Is Brightcom Group Limited’s (NSE:BCG) Shareholder Ownership Skewed Towards Insiders?”

BySimply Wall St

–

The big shareholder groups in Brightcom Group Limited (NSE:BCG) have power over the company. Large companies usually have institutions as shareholders, and we usually see insiders owning shares in smaller companies. Warren Buffett said that he likes “a business with enduring competitive advantages that is run by able and owner-oriented people.” So it’s nice to see some insider ownership, because it may suggest that management is owner-oriented.Brightcom Group has a market capitalization of ₹128b, so we would expect some institutional investors to have noticed the stock. Taking a look at our data on the ownership groups (below), it seems that institutions are noticeable on the share registry. We can zoom in on the different ownership groups, to learn more about Brightcom Group.

View our latest analysis for Brightcom Group

ownership-breakdown

NSEI:BCG Ownership Breakdown May 18th 2022

What Does The Institutional Ownership Tell Us About Brightcom Group?Institutions typically measure themselves against a benchmark when reporting to their own investors, so they often become more enthusiastic about a stock once it’s included in a major index. We would expect most companies to have some institutions on the register, especially if they are growing.

We can see that Brightcom Group does have institutional investors; and they hold a good portion of the company’s stock. This suggests some credibility amongst professional investors. But we can’t rely on that fact alone since institutions make bad investments sometimes, just like everyone does. If multiple institutions change their view on a stock at the same time, you could see the share price drop fast. It’s therefore worth looking at Brightcom Group’s earnings history below. Of course, the future is what really matters.

earnings-and-revenue-growth

NSEI:BCG Earnings and Revenue Growth May 18th 2022

Hedge funds don’t have many shares in Brightcom Group. Looking at our data, we can see that the largest shareholder is Sarita Commosales Llp with 5.2% of shares outstanding. For context, the second largest shareholder holds about 5.2% of the shares outstanding, followed by an ownership of 4.1% by the third-largest shareholder. Furthermore, CEO Muthukuru Suresh Reddy is the owner of 0.5% of the company’s shares.After doing some more digging, we found that the top 25 have the combined ownership of 50% in the company, suggesting that no single shareholder has significant control over the company.

While studying institutional ownership for a company can add value to your research, it is also a good practice to research analyst recommendations to get a deeper understand of a stock’s expected performance. As far as we can tell there isn’t analyst coverage of the company, so it is probably flying under the radar.

Insider Ownership Of Brightcom Group

The definition of an insider can differ slightly between different countries, but members of the board of directors always count. The company management answer to the board and the latter should represent the interests of shareholders. Notably, sometimes top-level managers are on the board themselves.

Most consider insider ownership a positive because it can indicate the board is well aligned with other shareholders. However, on some occasions too much power is concentrated within this group.

Our most recent data indicates that insiders own a reasonable proportion of Brightcom Group Limited. It has a market capitalization of just ₹128b, and insiders have ₹17b worth of shares in their own names. That’s quite significant. It is good to see this level of investment. You can check here to see if those insiders have been buying recently.

General Public Ownership

The general public, who are usually individual investors, hold a 47% stake in Brightcom Group. This size of ownership, while considerable, may not be enough to change company policy if the decision is not in sync with other large shareholders.

Private Company Ownership

We can see that Private Companies own 30%, of the shares on issue. It’s hard to draw any conclusions from this fact alone, so its worth looking into who owns those private companies. Sometimes insiders or other related parties have an interest in shares in a public company through a separate private company.

Public Company Ownership

Public companies currently own 4.1% of Brightcom Group stock. It’s hard to say for sure but this suggests they have entwined business interests. This might be a strategic stake, so it’s worth watching this space for changes in ownership.

Next Steps:

It’s always worth thinking about the different groups who own shares in a company. But to understand Brightcom Group better, we need to consider many other factors. For example, we’ve discovered 2 warning signs for Brightcom Group (1 can’t be ignored!) that you should be aware of before investing here.

Of course this may not be the best stock to buy. Therefore, you may wish to see our free collection of interesting prospects boasting favorable financials.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

May 20, 2022 at 4:34 pm #14007RajaRegistered BoarderInteresting to note a competitor of BCG an affle investor trying to run down the company….let’s not forget the info yet to be confirmed that the big bull is also buying into this….all in all possible involvement of relevant people including management may be involved in cornering a big chunk, post listing of bonus shares….

On the brighter side, I am holding a big chunk at less than 15 rupees and these dramas will be cleared by this month end. Kindly decide on buy or sell call by yourself.

Best wishes to all long termersMay 20, 2022 at 7:51 pm #14008JackSparrow13Registered Boarderhttps://www.bseindia.com/xml-data/corpfiling/AttachHis/37da8ec5-dbb6-4f8f-84b3-a2cfeee3caff.pdf

The above link contains managemnet’s reply on trade receivables.https://www.bseindia.com/xml-data/corpfiling/AttachHis/a267c6e6-edea-4d53-b179-5f9589c6f8ba.pdf

Slide 7 says

The target FCF for FY22 remains at Rs 250 cr, and as stated in earlier communication, is slated to reach Rs. 500 cr by June quarter, 2022. Improving Free Cash generation is a key financial target for management.Remaining Controversy about Promoter selling share

If you need capital to grow, you often sell shares. Often promoter holding in start ups, founder led companies (1st generation) are diluted to raise shares. Even Shark Tank is just that. Let my put a reverse logic, whats the need for a promoter to run the company day-to-day, when he holds a minority shareholding. Answer – It must be passion and devotion to the company. The ultimate solution of course is a stronger promoter share.I personally dont believe management should clarify to every Tom, Dick Harry’s article, who runs 20 ratios, and eventually writes about 5 financial metrics where picture seems most disturbing (over extremely long time periods). The name Brightcom gives cheap publicity, especially if you write a article against it.

What should management do

1. Focus wholeheartedly on business. Not lose focus on every new noise maker.

2. Maintain steady dividend, and steadily imporove over years. Atleast the the “idiots” like us, who are refusing to accept “market wisdom” should be rewarded little by little.

I draw attention to management commentary about dividend (1st link).

“We are a company that has grown through acquisitions, as a result that our stand-alone parent company is relatively small, and was more in the nature of a parent company ( this is changing now, with the beefing up of standalone operations at the parent level). Our standalone revenue is at Rs 365 crore as against consolidated revenue of Rs 2855 crore, in FY 21 . Over time, we intend to increase our dividend payout, as the standalone parent starts getting to a higher size and scale. Cash generation Divergence between holding company-type parent companies and operating subsidiaries, is routinely observed worldwide, in such normal corporate structures, since most/ majority, of the business is generated at the subsidiary level and not at the parent level, for such companies”

3. Over next 5-10 years, sort out shareholding issue.I have never seen such a concentrated amount of dirt being thrown on a company. Makes me more bullish on Brightcom. But portfolio allocation is vital. Have your limit on maximum you will want to risk on a particular stock, and stick to it. We are not employees of Brightcom…

May 20, 2022 at 11:08 pm #14009DograRegistered BoarderThe article in ET prime is written by Varsha Santosh. Varsha WHO? One can search Linkedin. I wouldnt glorify an “opinion” and open ended article from a nobody – ” stellar returns or just a mirage?”. She is questioning our company. And many like her are. So, the real question for me is – who really posed the assignment – ” How can you save some stupid retailers from BCG scam? Remember Sucheta Dalal? Good luck!” Mounting debt? Serously? Who proof read and gave a go for the article to be published.

One just needs to compare TTD, APPS with BCG. The business constraints are similar if not the same.

On top, our company also likes to inflict injuries to itself.

I have just one thing to say to SKR if I ever meet him (maybe I will soon) – You have a once in a lifetime opportunity. Dont blow it up with procedural/communication lapses. 28th May D-day! Time to shine.May 21, 2022 at 1:54 pm #14010kiranjRegistered BoarderBrighcom group Investor Conference Call

The company intends to conduct an Investor conference call on Wednesday, June 01, 2022, at

04:30 p.m. (IST).

This call will happen after the results announcement on May 28, 2022. The primary objective is

to present the results and the company’s future plans to the shareholder community12+May 25, 2022 at 6:17 pm #14011chrisRegistered BoarderGood volumes traded today, 5 large deals of more than 2,00,000 shares (2 on bse, 3 on nse).

One week to go to June 1st, for some info on the SHP.

8+May 27, 2022 at 10:30 pm #14015 -

AuthorPosts

- You must be logged in to reply to this topic.