Forum Replies Created

-

AuthorPosts

-

hw_twRegistered Boarder

Listing out some questions which are running in my mind over the weekend and the answers I am getting at this point of time

Q: Has the promoter REDUCED stake

A: YesQ: Has the promoter SOLD shares in open market

A: Yes and No basis different theories floating around …When we look at whole 18 Crs shares this makes it impossible to sell them in open market where the total transacted shares itself is only around 12 Crs

When we look at stakes separately of each Individuals / HUFs and other firms it could be that some transactions might have happened in open market and some in other routes like Share swap, Offline transactions or just moving out some existing promoter as non-promoter

Q: Have they reduced stake from 22.4 to 18.47 as reported in Money control or it’s 19.74 to 18.47%

A: It is actually from 19.74 to 18.47% … note that the reduction from 22.4 to 19.74% is due to increase in total no. of shares because of new preferential shares issuance to some LLPs along with Mr. SS plus MediaMint

In total the reduction is 1.27% … this might be significant for some and not so for some

Q: Why is this not reported to exchanges before … Can SEBI take some serious action on it

A: Reporting has to be done indepently by the party who did it … It’s not the duty of SKR to report on behalf of other promotersSKR has reported it directly or indirectly (whichever way we take it) on Apr 5th while updating LLPs acquisition and further inclusion as promoters

SEBI can put a penalty plus some fine basis the loss caused to investors … SEBI had penalised Redmond Investments before for not reporting their transactions

This also tells us that some of these Promoter group entities are totally not in control of SKR / VK and we can’t link their actions

In this case too they might put some penalties if proven that they have not reported it irrespective of whichever way the transactions are done

Q: Is this reduction in existing stake linked to their business … are the numbers going to be bad

A: Largely No … SKR published this new presentation at this point of time to address this concern and let people know that business is as usual… given that this reconfirmation of 500Cr FCF came after Q4 we can be rest assured that Q4 revenues is in-lineQ: Is this reduction linked to future earnings … are they expecting some drastic reduction

A: No, in that case why would they increase the stake back and bring in the LLPs as promotersQ: Is this reduction in existing stake linked to FA … are they expecting some huge impact

A: Probably and partially No … As we can see above that business is not impacted and most importantly the reporting mechanism is not going to change in future that would impact topline and bottom line numbersAlso we need to recall Mr. SS’s full payment

Q: Why have they reduced existing stake first and increased it back with new stakes from LLPs … What was the need to do this Rejig

A: I guess this is the most important question everyone need to ask themselves and seek answer forI might be totally wrong in this … My guess is that SKR has done it to protect the company from any HOSTILE TAKEOVER by any third parties acquiring these LLPs and other new LLPs as well or by any other route … Since the cash required for it is huge, SKR and few other promoters might have taken this option to part away with their existing stake and get some cash and use it to acquire these LLPs (I guess Satyamite mentioned this too)

Q: Is there a chance of increasing stake in future

A: Probably Yes … basis Satyamite’s logic it can go around 24%The other option is to get into these fresh Preferential allottee LLPs assuming that they have enough funds left (atleast VK’s portion) to purchase this stake

Or include some of these large Individual Investors as promoters … We all know that Mr. Subrato Saha ex director holds significant stake both individually and through his firm … Given their friendship isn’t it simple enough for SKR to make him as promoter … Even if not done he is still as good as promoter holding his stake … Similarly there will be some more other investors like Mr. Peshwa Acharya’s family who can be included in promoter group

Or they could openly purchase from the market

———Selectively picking up and linking some events like Stake reduction, FA etc; might not give us correct picture, especially ignoring other events like Significant stake increase back through LLPs, MR. SS’s investment, Business intact, Acquisitions intact, Numbers, FCF intact, Possibility of future Stake increase etc;

As small investors we might not get answers for some of these questions in future too and thus puts us as the most riskiest lot of investors … It is important that we listen to everyone’s point of view and try to ask more right questions and be open and take our investment decisions basis our individual risk appetite

Note that these questions are important and these answers are just my views at this point of time basis what I am reading / understanding at this point of time and subject to change as things unfold and I might end up not even expressing it over here

hw_twRegistered BoarderMy views on recent March SHP

Negative

– Promoter reduced stake by around 1.5% overall … this is not a good signPositives

– Pledge percentage decreased

– FII / FPI percentage IncreasedFuture Hope

Similar to the recent event of SKR becoming partner of 4 LLPs there are chances of he becoming partner in other LLPs too and eventually increase promoter percentage … this is just a guess, we need to be careful till that timehw_twRegistered BoarderBCG should have appointed a new CFO by now as they were aware of this exit

This thought crossed my mind the very first time when I heard this news and I felt they should have closed it by now, but when I thought for a while and I recall some of my hiring experiences in corporate world I feel it is rather common to have delays in hirings … the challenges arise from multiple angles, in terms of finding the right fitment and many other external factors which are not in your control

In terms of right fitment, some specific challenges this position brings in

– One person – This is a single person post heading a team and not a team member position where in you can hire and still live with that person even though the person is not upto the mark … You need to be extra careful making sure that the person is the right fitment in all aspects

– Face of the organization – He will be the face of the organization representing it in multiple forums like in Analyst meets, Investors calls, Mergers & Acquisitions, Nasdaq Listing, Road shows etc; … and especially give that BCG is fast growing, touching Billion dollar in sales with operations expanding in multiple countries he would be required to have a good understanding of latest technology, legal compliance apart from accounting standards and systems followed across the world

– No replacement – As mentioned above, you just can’t hire and fire as it is not only waste of time and money but also reputation of the company will have a huge impact apart from many others

– Connect with the business – For the CFO to stay long, he needs to connect with this AdTech business and believe in this growth story … Its like a co-founder position where the person is connected to the business right from the beginning… In this case SKR has to make sure the new CFO is connected and carries the same passion as the founders

Huge delays happen when it comes to tech people hirings irrespective of levels … It gets delayed because of HR policies like 3 months notice and the candidate declining offer in last minute or not turning up even after accepting offer … I guess this problem may be there to a certain extent even in Finance people hirings … Apart from this budget is a big problem in tech hirings and most of the times we need to increase it just to close the position in time

Note that the official FA news came in around a month back and I am sure his exit and replacement would have been planned even before that … I attribute this delay is purely because of finding some right fitment and some typical recruitment challenges

Having said this, I feel BCG could have scored some brownie points had they announced a new CFO along with the exit … they still can and hoping they will with some right hiring …🙂

Anyway, it is mentioned that they have shortlisted few … hoping they find some good quality and reputed people taking the mantle from YSR and steer the organization to greater heights …💲

hw_twRegistered BoarderIs there any link between FA and CFO’s exit

My view is clearly NO for the following reasons

– CFO has RETIRED as he has crossed age limit and has not RESIGNED

– There is no timeline set for FA completion … It can take few weeks to many months as seen in other cases

– Holding someone for another few weeks or months is clearly not an option … Corporate world prefers certainty about the dates so that they can work towards finding a replacement … It a difficult process and takes lot of time to find replacement (will discuss this later)

– Lastly we are not aware of his Health condition and his ability to continue even if the company wants to … I am happy that BCG has taken an employee’s first approach by not holding an employee for whatever reasons especially when someone has worked for such a long period … he doesn’t deserve any kind of pressure tactics from the company for whatever reasons and would definitely needs a graceful exit without any hurdles

This also sets a right example for the new comer as they can join confidently with full knowledge of what’s happened about FA and how company has treated employees even in difficult situations without holding them to stay in the company for their benefits

Thanks YSR gaaru for all your valuable contributions behind the scenes and wish you a Happy and Healthy life ahead

hw_twRegistered Boarder@vstvm1981 – Vanguard ETF which was tracking FTSE Global Index has purchased most of these stocks on this Thursday

Basis the volume spike (of 1.3Cr which at some point went to 1.5Cr+ at the upper circuit) we can assume that the same Vanguard fund has also tried to get BCG too but they couldn’t get it as by that time there were already some 40 to 45 lakh+ shares pending in queue at the Upper circuit

I guess they would try to purchase it again from Monday onwards … hopefully they try it in the morning itself instead of last one hour

We can check Vanguard deals over here from StockEdge website

https://sedg.in/7i9bd1neOne more thing, they had purchased more number of stocks than what was mentioned in the below list …

FTSE India rebalances today at the close (last 30 mins VWAP).

Largest inflows on $YESB.NS $TTEX.NS $PERS.NS $DPNT.NS $DIXO.NS $TBEI.NS $MAXE.NS $TTML.NS $DLPS.NS

Largest outflow on $SNFN.NS

Inflows on $IIFW.NS on Monday.

For more, see https://t.co/pS06x9tJBO pic.twitter.com/lZtL7jefc1

— Brian Freitas (@tradingarb) March 17, 2022

For example, 15.45L+ AngelOne shares vs 6.7L initial expectation … Hoping they would do the same with BCG too

hw_twRegistered BoarderThe Audit outcome is not going to change irrespective of whether the Audit has started long back or last week or whether the Audit will take 72hrs as mentioned by someone in MMB or some 6 months plus

Similarly Audit outcome is not going to change because some FII is still buying out there or if in case Mr. SS decides to wait and watch or he does a full conversion

Also it’s not going to change just because MediMint acquisition is thru or by Releasing earnings Guidance or some other action of the company ( No doubt all these are Trust boosters )

Also it is not going to change just because the price is falling or raising

It’s not going to change just because 2 lakh investors Trust and few investors doesn’t Trust

We need to just let SEBI and Deliotte do their duties and let BCG’s management continue their day to day operations as is without bothering or blackmailing them … In the end, We need to Accept whatever Deliotte report as is

Meanwhile, the question in front of us is … do we believe in the numbers or not …

If YES, stay PUT and wait for the Audit Report as and when it comes

If NO, we need to understand what is the Risk involved … Is this a big one or a small one … I mean will they consider this as an intentional misrepresentation of numbers or an unintentional one with just some observations and corrections along with some guidelines to follow

Also we need to note that the checks are only about impairment component … As we heard from many Accounting experts that this item is just an accounting entry and there is no cash going out from BCG’s Banks … meaning even if something comes out there is nothing to worry about as there is no question of money siphoning at all

In my view, the interpretation of these entries are subject to accounting standards of that country and are always debatable … Its going to be EY vs Deloitte… At most Deliotte will be issuing these observations and asking the company to make necessary corrections and follow some standard guidelines and nothing more than that

This is just my view basis my understanding at this point of time … Request all investors, not to get carried away with just price movements as it doesn’t reflect anything at all … please try to understand the matter in detail on your own and evaluate your own Risk … Accordingly you can take a call whether to Buy or Sell or Partially Sell or Just Wait and Watch

hw_twRegistered BoarderRequest everyone to please read it in detail … NASSCOM the industry body for corporates has already raised its concerns to SEBI stating that

– There is no need to Intimate exchanges on Initiation of Audit … as it is a huge Reputation damage and Capital loss to the company ( this is exactly what we are witnessing in BCG’s case )

– Also it is against existing SEBI rule as the event is not yet “Materialistic” event … meaning it doesn’t need to inform anything till there is a final Audit report

As I said in my last post, there was no corporate governance issue from BCG … NASSCOM has raised the exact concerns on the damages that would happen to a company with this rule

Hope people try to understand things from corporate point of view and stop debating atleast on this point

hw_twRegistered BoarderI don’t think company can satisfy investors with another update or even a call … On the contrary it might create further confusion

Most of us are still stuck our minds out there on past things like company should have informed us before on Sept 16th itself … and some people have tried to justify this fixation further that company would have done some hera-pheri and that’s why they have delayed this communication etc; and other theories

Nothing can change these fixed minds except the final Audit report for which we need to wait for long

The more questions we ask, the more suspicious we start getting into … company can’t share each and every detail with us as they do with SEBI and Deliotte

Company has already given an update on sequence of events that have happened and the next course of action from Deliotte … Also previously they have already given details of list of Assets that are impaired

Some Facts which we need to Accept as is, as the things stand right now

– The company is undergoing a detailed Audit … It doesn’t matter now whether it has started on Sep 16th or Feb 25th

– The company has informed exchange as it is mandated by SEBI … Its a huge reputation impact which any company has to bear … If not for SEBI’s mandate no management would ever be willing to inform investors at this stage as it is only the beginning of the Audit … the last two days of reactions and price actions is a clear evidence of the situation which any company doesn’t want to get into

– There is no evidence of any hera-pheri yet

– There is no financial impact because of these wrong entries

– There is no timeline fixed by SEBI … and it is also difficult to fix any timeline given the complexity of it and the multiple parties and multiple iterative steps they have to get into to arrive at final report … The Audit can go on for 3, 6 or 12 months

Even Deliotte will not be in a position to give any timeline

There is no point in keep asking the company for an update and infact there is nothing which a company can update us apart from saying “The Audit is going on and we will inform as soon as there is an update worth enough to be informed” …🙂

Instead of getting into never ending questions mode, its better that we focus on following things

– Suggest possible actions actions (except another update) we seek from the company so that the Trust can be built …

Like closure of Media Mint acquisition soon, Releasing Guidance numbers early etc; and some others as suggested by one member in Telegram channel– Focus on the happenings on the business front during this period

– And finally Wait for the Audit report

hw_twRegistered BoarderPresentation on Impairments from BCG shared to exchanges back in July 2020 … Sharing it again for the new knowledge of new investors who had entered post this event

The impairments is a clean up activity done by the company and is across its 10 subsidiaries

– For Products, tools and datsets which are as old as 12 years ago and obsolete and also has regulatory challenges like GDPR

– Advances paid to Publishers … couldn’t recover them fully as there was less traffic to these sites

– Advances to colocation centres

Attachments:

hw_twRegistered BoarderWhat is GDPR in layman terms

It is a privacy law defined by European Union / EU to protect privacy of users sharing their personal details to a particular company like FB, WhatsApp, Telegram or even this website

As per the law, the company collecting personal sensitive information like name, age, email-id, phone numbers, aadhar, pan etc; should do so with certain conditions that they are going to protect it end to end and also won’t share it with others for any type of usage including marketing / ads … This also applies to companies who get this data from 3rd party for processing and to companies who deal with data from EU

For example if you have uploaded your resume to Naukri … GDPR law strictly prohibits InfoEdge the parent company of Naukri to share this information for their other portals like 99acers or PolicyBazaar or Zomato etc;

In another example, Facebook previously shared their data to a firm called Cambridge Analytica which in turn used it to influence voters during Trump election … FB was fined 5 billion dollars for this breach

In case if there is any breach, the company is liable to pay 4% of their turnover

BCG has impaired certain Assets which they felt it is not worth in the context of GDPR compliance …

The Asset they are referring to could be a Software or Data collected using their own Software or from 3rd party or a Hardware storing this data or all of theseBCG would have all these legacy assets valued at certain value over a period … Note the valuations could be both the cost of building / purchasing these Assets plus Good will … They might have found that these assets are no longer complaint to GDPR

They now have options to modify them or sell or discard them … and they have choosen to discard them also assuming that there are no customers for these assets and also they can’t sell them in the market as the target company will also have the same challenge 🙂

Coming on to the penalty portion it is 4% of your turnover every year … Let’s say BCG is charged after 3 years … it would have to pay minimum of 200 Cr for every year and for 3 years it would range anywhere from 600 to 1000+ Cr … this amount they have to pay irrespective of the benefits they got like even for 1 rupee

Now decide why would anyone want to keep certain Assets which are not worth for and are not used by them … Isn’t it better to discard them and clean your books

hw_twRegistered BoarderWhat is the scope of the Audit

BCG has already clarified that the matter is only related to the Impairment of Assets and nothing beyond that as we perceived from Sept 16th letter … this is good in terms of timeframe and costs if any on BCG side … It is good even in case of a full fledged Audit tok but just takes more time and thus more concern from impaitent short term Investors

What is the timeframe of this Audit

It took 5+ months to do the initial check … I guess Deliotte may not be fully involved all these days … Assuming the scope is more clear now and they also had most of the documents on their side, I feel it might soon get closed … can’t say the exact time, but generally these firms work on a fixed timeframes and also push their clients to share the documents soon so that they can close it within the timeframe

Another view is that for the recent acquisitions by BCG, EY and others were taking around 2 months to close the financial due diligence … This might also take similar time or lesser as the scope is only pertaining to Asset Impairment

What is the impact of it if they find out any thing

– Revert the asset impairment partially or fully

– Penalties to Management plus something more probablyBefore that I guess BCG will have option to contest the findings

Will there be any financial loss to the company

Since these are non cash items, and just a book entries I guess there won’t be any material impact

Please note, these answers are just my views and may not be fully correct … But the questions are more important for the investors to focus on and get answers for

hw_twRegistered BoarderWe are unnecessarily getting worried about matters which are not important … information is shared to exchange when the matter is clear from SEBI that they would want to go ahead with the audit … let’s look beyond this

Now the question is Why SEBI wanted to go ahead with the Audit … Is SEBI/ Deloitte not satisfied with the information shared all these days ?

From SEBI’s point of view they are not the authorities to certify that the accounts are clean … their job is to protect investors by taking actions … For this they have hired external Auditors like Deliotte to dig into things in detail and find out if the accounts reported are as per the law

For example in this case SEBI will not have any clue on what GDPR compliance is all about and how it will impact the organization … also I guess they will not have detailed knowledge about country specific accounting standards

So SEBI has offloaded their Risk to third party … They will play safe and rightly so to protect themselves from any damage caused because of wrong findings … tomorrow no one can question SEBI that you gave a clean chit

Its like doctors / hospitals saying that you have Cancer or some other problem basis Diagnosis / Scanning report findings and not on their own … later on when we figure out that there is no Cancer through some other means we can’t go blame a doctor that your diagnosis or treatment is wrong

Now the second question is Why has Deliotte not satisfied with the information shared … Why they want to get into an formal engagement

One reason which I could think is that it is more a operational issue forcing them to get into a formal engagement

The current Deliotte team would be looking at things at high level and may not be fully equipped to deal this matter on their own … This team will have knowledge in Indian accounting standards only and also will not have much idea about GDPR

Now that they have the initial set of documents they know that they would need to also involve other country specific auditing team and also the experts who understands GDPR law

In this case they would need to involve teams from Israel, Argentina, USA and also the teams who has knowledge in GDPR

Note that they can’t involve these people just like that … All these people are billed on hourly basis and their rates are pretty high … these individuals allocate their time for an engagement only if there is a formal contract … Now that they have the scope clear after the initial discussions with BCG team they can get into a contract for the Audit and close it

In short SEBI is dependent on Deliotte India Audit team … and Deliotte India team is dependent on other country Audit teams along with GDPR experts

hw_twRegistered Boarder@Brightspot – Actual Auditing will be starting only after the Feb 25th letter from SEBI.

The initial letter was only a intimation to the company … All these days BCG was contending the matter that the audit was not required as this impairment is because of GDPR compliance and is a common practice for internet companies.

Ii is only in the abot context, the company has shared some documents to both SEBI and Deliotte. Just because it started sharing information doesn’t mean that Audit has started.

There was no need to inform exchanges on Sept 11th as the matter was not finalized and only talks were happening

Please read the Original text again

“The company represented to SEBI that the said audit was unnecessary because several internet

companies had to take such charges globally, owing to the GDPR norms.Since September 2021, the company has extensively cooperated with SEBI and the Auditor, in

this regard, by supplying volumes of data, such as below:”This confusion is because the company has shared only the Sept 16th letter and not the Feb 25th one … I am not sure for the reason behind it … Probably the final intimation was in the form of mail chain with some other information which is not relevant for investors and BCG might be waiting to receive physical copy to be shared to exchanges

hw_twRegistered BoarderLast couple of weeks was a eventful period for BCG … Summarising some of the updates which I could recall

Investor updates

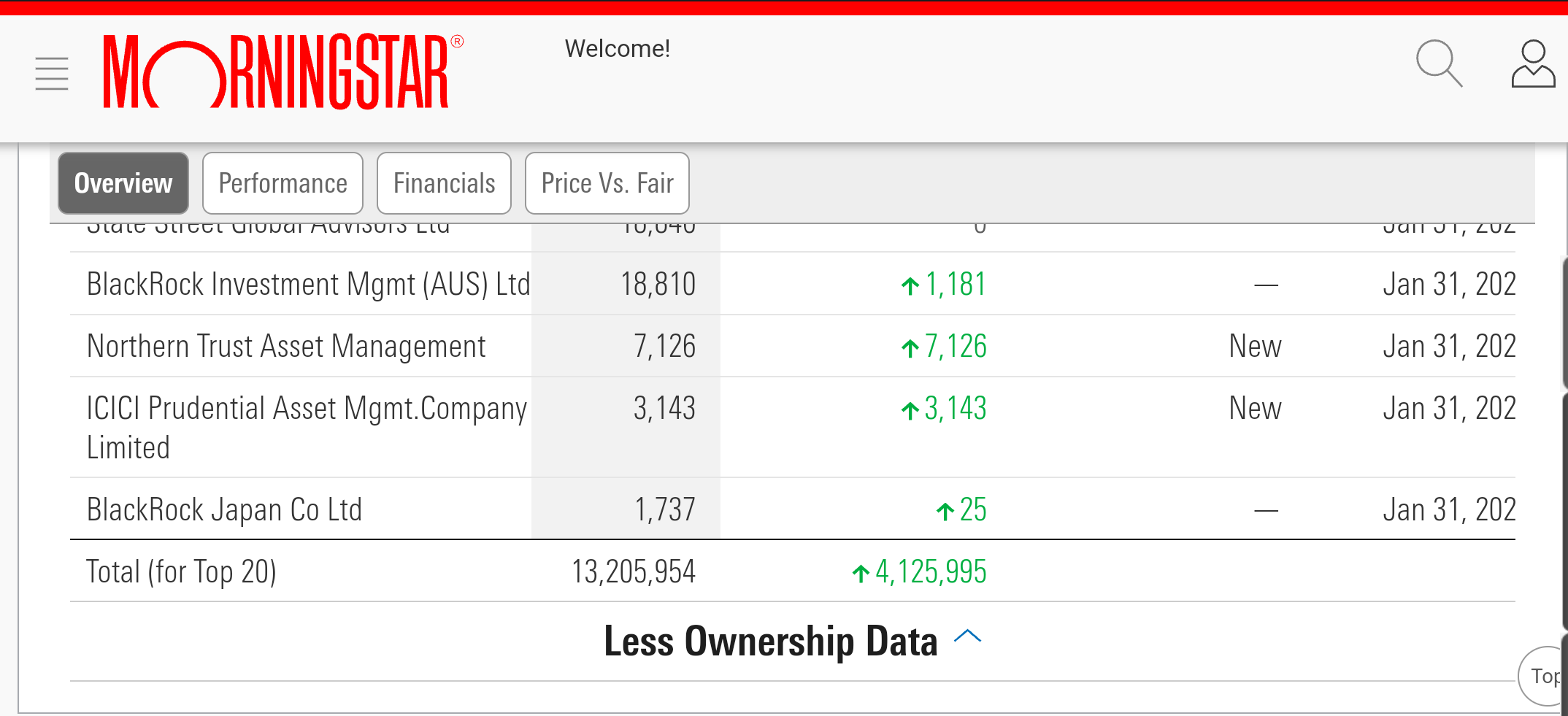

– Around 15 lakh shares added by Fund houses in last one week … Morning Star shows count of 1.32 Cr compared to 1.17 crore shares last week

– BCG is added to the NSE Indexes

Nifty 500

Nifty smallcap 250

Nifty smallcap 100

Nifty midsmallcap 400

Nifty Total Marketeffective from March 31 (Src: NSE) … This would increase the coverage from Analysts, Media and also would mark entry of new MFs in near future

– BCG is added to FTSE Global All Cap Index effective from March 16th … I couldn’t find public info about this, if anyone has please do share a link … If true, Vangaurd ETF would be adding this stock around these dates

– As per Economic Times, Rakesh Jhunjhunwala has invested in BCG … some tweets were put across to ET to confirm or correct the news … they haven’t done both even after 5 days … So please take this news according to your own study

– Record date for bonus issue is set to March 16th … expecting Mr. SS do a conversion by paying the remaining 75% amount before this date

– e-voting for Bonus has ended on 27th … Results announcement expected today

– BCG is covered in CNBC TV 18 channel … SKR appeared in a news channel after many years … hoping to see more media coverage in coming months

– BCG is also covered in couple of Groww YouTube videos

– BCG ranked 21st in Dalal Street Investment journal’s list of Super 50 stocks … This is based on Growth, Effeciency, Safety and Wealth creation parameters … BCG is just behind Infosys and Persistent Systems which are ranked at 19 and 20 respectively

Business / Operations updates

– BCG has launched a new product named B-Finance with well known publishers like Motley Fool … this is a good move considering the audiance of these sites are highly focused and are willing to pay to earn … the conversion rates will be high and thus CPM rates too

– Brightcom Israel has closed couple of positions for their Brightcom Video player division including Head of Video product … hopefully we will soon get some business updates on this product

– Brightcom Israel has 4 positions open (Src: LinkedIn) … 1 new position for India added in this week … Once closed we might see some increased revenue from India

– MediMint has 15 total positions open … 3 new positions added in this week including one position in US (Src: LinkedIn)

Attachments:

hw_twRegistered BoarderWhy there are no MF investments in your company?

Are we looking for a validation that if MFs are investing then company is good otherwise it is bad?

Please also ask yourself some other questions

– Why foreign investors are investing and why Indian MFs haven’t yet entered in big way … are FIIs bad judges of stocks

– Why ICICI Prudential has entered recently and why not before at lower price … Is ICICI a bad judge of stock picking and other MFs are good or vice versa

– Why Mr. Shankar Sharma has invested and why not others

– What about MFs who have invested in many wealth destroyers like Unitech, Suzlon, HFCL in 2000, Reliance Capital, Communication and all ADAG stocks in 2000s … there are many others which MFs have invested when the stock prices are in peak and with high valuations … One more example of all recent IPOs with abnormal valuations and heavy investments of MFs in these companies and in the process also luring lot of innocent investors who are relatively new to the market, initially in the form of IPO and later in the form SIPs … Who would take responsibility for this debacle

“MFs are subject to Market Risk” …

There is no guarantee that MFs are risk free and would invest only in good companies … There are many funds which have destroyed wealth too, but no one talks much about that

Same is the case with Marquee or FII investors too

There is never a guarantee that investments by any of these parties means this company is good otherwise it is bad

If you believe that MFs are zero risk and you want to invest only when they had invested please continue doing so and stay away till your event is triggered … but don’t assume and paint a picture that the company is bad just because someone has not yet invested

Listen to everyone both negative, positive and balanced views from people like Logan, CI, Headstead and many others … But, in the end you have to make your own investment decisions … don’t live on a borrowed conviction

hw_twRegistered BoarderThe question related to high receivables of 1400 Cr is actually for Sep quarter

Foor Dec quarter this number is around 2000 Cr … It indicates these things …

– The questions were prepared long back, but at that time the sentiment was positive with price rising and they were waiting for the right time (price falling) to conduct this interview and ask these questions just to prove their point … Also clearly visible with their tone and rudeness

– The interviewer hasn’t bothered to update the question or was just lazy and copying it from someone’s questions list

– Interviewer also said “there are handful of other problems as well” … indicates their pre-determined view about the company

Coming on to the receivable days, In the last conference call Mr. YSR, CFO of BCG has clearly mentioned that these receivables are largely pertaining to the latest Q3 quarter business …

This means there are no bad receivables … In my view, this is absolutely fine considering the nature of the business … Anyway, this will be decreasing in coming quarters as their sales come down because of seasonality of the business

Also as I mentioned before this is actually positive and advantageous to the company compared to their peers …as now that the company is able to overcome this high working capital and receivable days requirements and is able to generate FCF too

If you are comparing this Working Capital and Receivable Days with a Software Services company … generally they get some upfront payment and some part payments based on milestones achieved

For example, let’s say there is a 10 Cr order … the payment terms will be like 10% upfront, 20% on milestone 1, 30% on milestone 2 and final 40% on final delivery and acceptance … The acceptance period will be for 2 to 3 weeks, post that there will be around a month for the final payment … So in most cases they will be getting final payment in the same quarter of work completion … If you calculate the he receivable days it will be one or max two months

Also in this case there is no other working capital need apart from employee salary expenses

But, in case of BCG their business is different and works differently … they have to make an upfront payment to Publishers to purchase inventory / ad slots … They then sell (or rather agree to consume) this inventory to Media Agencies or Digital Marketers or directly sell it to brands … the payment periods would differ for each of these parties and is higher for Agencies as they have to in turn sell it and get their payment post the actual consumption of ad slots

The sequence of events and their possible time frames are give below … (Disc: I am a s/w person and my knowledge in this business is limited … there could be some errors in my understandings)

– BCG purchases bulk inventory / ad slots from FB … Day 0

– BCG sells a portion of this inventory to Media Agency … Timeframe 1 to 7 days as they would have already purchased it basis prior inventory demand from Agencies and other customers

– Agencies sells this inventory to Digital Marketers or Brands … Note that these transactions between BCG and MA, DM and Agencies are not actual sales, they are just agreements allowing brands to “consume” their inventory … Timeframe of 1 to 2 weeks

– Brands / DMs run a campaign … Timeframe of two weeks to more than a month depending on type of campaign

– Final result is evaluated in terms of actual consumption, quality … the real consumption is agreed between the parties … Timeframe of week or two

– Invoice is raised at the end of campaign or for a set of campaigns at the end of month or quarter and the payment is received in few weeks to month post that

Note that payments are received from Brands to DM first … Then DM to MA … Further from MA to BCG and again there is a time delay from invoice to actual payment between these parties

As you can see above the time delay is because of multiple parties involved and the final payments are happening only after the actual consumption of the inventory and not on mere agreement of consuming it … All this also leading to high working capital as explained by SKR

Hope we understand and agree why BCG has high working capital needs and high receivable days

In other real world metaphor … Its like a Rice Miller getting paid after the end customer has actually consumed rice … 🙂

In more detailed explanation … Its like a Miller purchasing it from farmer at a discounted rate with upfront payment … Miller then sells it to wholesaler … who in turn sells it Retailers … who inturn sells it to end customers … and the customers pays back ONLY after Consuming rice at the end of the month provided feedback / quality is matching to initial promise by the retailer

Imagine the amount of working capital requirement and receivable days of the Miller in this business scenario … 🙂

hw_twRegistered BoarderWhen you have not done a detailed study of the company, its business model and the history … you will end up with questions with lot of ambiguity … and also you will not be in a position to understand the answers provided by the other party

Regarding question related to BCG’S biggest clients …

BCG directly and indirectly works with different parties … Like Publishers, Media Agencies, Digital Marketers, Brands etc;

In this context, it becomes tricky to understand what the interviewer is exactly looking for … I mean, is the interviewer asking large clients in terms of a big names across these different types of clients or only from a particular type and is the question is about large client in terms of big brand name in general or a big brand name which the interviewer is aware of (like Google, FB, Unilever etc;) or large client in terms of revenues

SKR has answered this question with the names of Media Agencies they are working with like MediaCom, Havas, Mindshare … But the interviewer could recall only names like Google, Yahoo, Unilever which they know

Also some of the questions indicates that they were not prepared well … Or they have a pre-determined judgement … and were also rude by not allowing SKR to answer questions … Will discuss this further

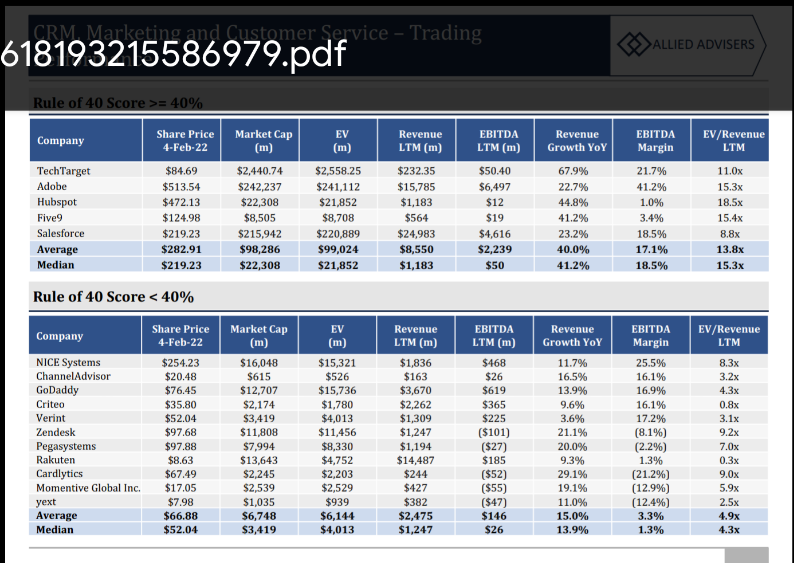

hw_twRegistered BoarderBCG’s last 12 month’s growth + EBITDA margins is way above > 40%.

As per the Rule of 40 for SaaS companies, BCG’s valuation should be in the range of 13.8x to 15.8x EV

BCG has clocked 4479 Cr sales in last twelve months (LTM) … Its valuation should be in the range of 61,810Cr to 70,768Cr

hw_twRegistered BoarderSet of events from BCG in next two months

In next one month

– Closure of MediaMint acquisition post cash payment– Bonus record date announcement

– Mr. Shankar Sharma’s balance 75% payment for warrants before the bonus record date

– Investors presentation from SKR as stated in the concall

– Earnings, FCF, ROE guidance figures from SKR for the next FY

In next two months

– Announcement of Audio AdTech company acquisition post closure of legal, financial due diligenceWe might hear some more news items like BCG inclusion in different other BSE, NSE indexes, FIIs / MFs additions, MF research reports, Leadership hiring, Product updates etc;

hw_twRegistered BoarderA wonderful discussion with Aditya Vuchi on his MediaMint’s journey and the lessons learnt in building a 1500 people / India’s the largest Digital Marketing agency (did he said that ..😉

Lot of insights to learn from, whether you are a startup person or a investor especially a BCG investor … I really liked the clarity of thought he has

Request everyone to please watch it and also share it

Teaser … He talks about US vs India business, Services vs Product business, Market size, Profitability, People, Strategy etc;

-

AuthorPosts